Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

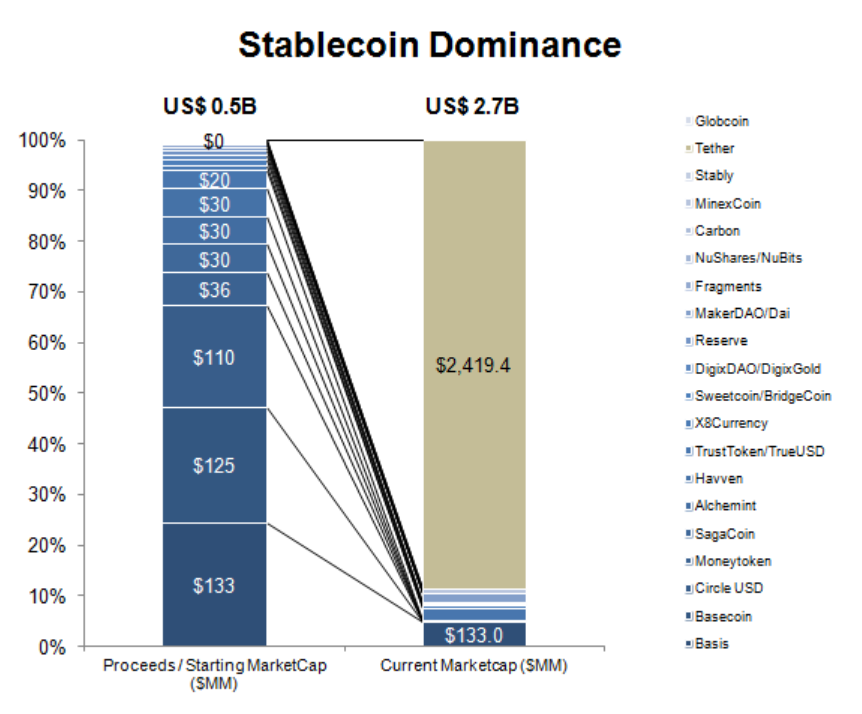

According to proponents of stable coins, the volatility of bitcoin and other cryptocurrencies is one of the biggest barriers to mainstream adoption. Stable coins come with the promise to remove these barriers and are therefore praised as the Holy Grail of Crypto. As of the time of writing, stable coins have reached a market capitalization of USD 4 billion. With the rise of decentralized exchanges without links to the traditional financial system, this amount is likely to increase. Despite the overall success of stable coins globally, none of the big projects has been listed on cryptocurrency exchanges in Japan yet.

In the following, we will explain the different types of stable coins and assess the regulatory environment for each model in more detail.

“Stable coin” is an umbrella term describing crypto assets which are stable relative to a predetermined asset – most commonly the US Dollar. In general, there are three types of stable coins: IOU[1] models, on-chain collateralized models, and seigniorage models.

The examples used in this article are for illustrative purposes only.

IOU models currently dominate the stable coin landscape. This is likely to be attributed to the simplicity and clarity of the model. While a look under the hood shows significant differences in design, all IOU models have in common that there is a central entity that issues tokens which represent a redeemable certificate against the issuer for the benefit of the token holder. To ensure the stability of the token, each token is generally fully backed by a fiat currency or another real-world asset. In few cases, a mere guarantee is made by the issuer to buy back tokens at a predetermined price.

In the case of TrueUSD, tokens are freshly minted when users wire funds to a third-party escrow account and burned when US Dollars are redeemed. This mechanism ensures parity between TrueUSD in circulation and the US Dollars held in escrow accounts. A similar mechanism is deployed by Libra[2], where each token is backed by reserves. New tokens are only minted if authorized resellers inject money into the reserves. Conversely, tokens are destroyed when demand contracts. Since the tokens are backed by a basket of fiat currencies rather than a single fiat currency, there will be fluctuations in price as a result of FX market movements.

Tether – by far the most successful but also one of the most controversial stable coin projects[3] – mints new tokens irrespective of user payments. Yet, similar to TrueUSD, the project promises to maintain a one-to-one ratio between its stable coin USDTether and US Dollars held as reserves.

In Japan, a project known as JPYZ was launched in 2017. Unlike the projects mentioned above, JPYZ are not backed by Japanese yen. Parity with JPY is maintained by a guarantee of the issuing entity to make a purchase order of each token for a price of JPY 1 on listed exchanges. The project is described as a social experiment and has not scaled as much as some of the USD stable coins yet.

Token(s): stable coin

On-chain collateralized models require a complex system of smart contracts, different kinds of tokens, oracles, and external actors to ensure their coin remains stable. MakerDAO, for example, requests its users to transfer crypto assets to a smart contract. The smart contract then issues a loan in the form of stable coins (DAI) and effectively locks the collateral in the smart contract until the loan is paid off.

The target price for DAI is set to USD 1 and used to determine the value of collaterals locked in the smart contract. Given the volatility of the collateral MakerDAO requires all loans to be over-collateralized. Where the collateral-to-debt ratio falls below a certain threshold, the position is automatically liquidated, and the collaterals sold on the market. This ensures that DAI always remains stable relative to the US Dollar.

A second type of token – Maker Token (MKR) – is used for the payment of a stability fee. This fee must be paid in addition to the debt in order to release the collateral from the smart contract. MKR tokens further play a central role in the governance of the Maker Platform, by giving each token holder voting rights (e.g. for the appointment of oracles and the determination of the stability fee).

Main tokens: stable coin, hybrid governance / utility token

Seigniorage models are based on the quantity theory of money. To keep the token price stable compared to a reference currency or another reference value, the token supply is adjusted continuously depending on demand and supply. In phases of inflation, the token supply is contracted automatically to bring prices back to the original level. Conversely, the token supply is expanded in phases of deflation.

In the case of Basis[4] the stable coins (Basis) were pegged to the US Dollar. To maintain the peg, the Basis supply was controlled by additional tokens – share tokens and bond tokens. The bond tokens were auctioned off for prices less than one Basis when the supply had to contract. When the system determined that an expansion of the Basis supply became necessary, holders of bond tokens received one Basis for each bond token in a first-in-first-out order. In cases where the bond tokens were not sufficient to expand the token supply, holders of share tokens participated in the issuance of new Basis according to their overall share tokens in the system.

Main tokens: stable coin, bond tokens, share tokens

In the following, we will analyze each model in more detail. Where a model involves more than one token, the additional tokens are considered in our analysis as well.

In an IOU model, a single token – the stable coin – is issued. Depending on the design of the token and the underlying business model, a token might either be classified as a prepaid payment instrument, money order, or virtual currency.

The Payment Services Act (‘PSA’) defines prepaid payment instruments inter alia as signs which are recorded electronically in exchange for consideration. Depending on whether the signs can be used for the purchase of goods and services from the issuer or the issuer and persons designated by the issuer, a prepaid payment instrument may either be classified as a prepaid payment instrument for own business or a prepaid payment instrument for third-party business.

In most cases, stable coins do not constitute prepaid payment instruments since they are not issued for the purchase of goods and services within a predefined ecosystem. Instead, they can be accepted for payment – irrespective of contractual relationships with the issuer – by anyone. The mere fact that stable coins can only be redeemed by users who have passed the know-your-customer procedure of the issuer does not lead to different results.

Also, the fact that stable coins issued under the IOU model can generally be redeemed for fiat currency speaks against the classification as a prepaid payment instrument. According to the PSA “issuers of prepaid payment instruments must not make any refunds” except in cases specified in the PSA. Typical cases are the redemption of small amounts and cases where the user cannot continue to use the prepaid payment instrument for inevitable reasons (e.g. discontinuation of the business of the issuer).

Stable coins issued in exchange for fiat currencies that can be redeemed by the token holder are likely to be classified as a money order. While there is no legal definition in the PSA or the Banking Act, a money order is commonly understood as a payment order for a certain amount of money. The amount indicated on the money order must generally be paid upfront and can only be cashed by the person shown as the recipient in the money order. Tokens issued under the IOU model do however, not include a recipient. Instead, they may be redeemed by anyone who owns the private key corresponding to the respective token. As such stable coins are comparable to blank money orders with enhanced safety features and increased negotiability. Even slight changes to the underlying business model may lead to different results (see item 2.1.3 below).

Tokens that are classified as money orders are not regulated themselves. For entities involved in the sale, transfer or redemption of the token, the law may require, however, that these entities hold a banking license or are registered as a transfer service provider under the PSA.

In some cases, stable coins issued under the IOU model may also constitute virtual currencies. The PSA distinguishes between Type I and Type II virtual currencies. Type I virtual currencies are defined broadly as property value that

Type II virtual currencies are defined as values that can be mutually exchanged for Type I virtual currencies with unspecified persons and which can be transferred electronically.

Currencies and currency denominated assets are explicitly excluded from Type I and Type II virtual currencies.

Since stable coins issued under an IOU model are likely to be classified as currency denominated assets, they cannot be classified as Type I or Type II virtual currencies.

Even slight changes to the underlying business model may, however, lead to a completely different result. This can be seen from JPYZ. Different from the other IOU models, JPYZ tokens are not refunded by the issuing entity but bought back for a guaranteed price through an exchange – JPY 1 for JPYZ 1. This has led the Financial Services Agency (FSA) to classify JPYZ as virtual currencies within the meaning of the PSA.

Entities issuing stable coins that constitute virtual currencies must register as a virtual currency exchange business in Japan.

On-chain collateralized models typically involve more than one token. In the case of MakerDAO, this includes a stable coin and a hybrid utility governance token.

Stable coins issued under an on-chain collateralized model are likely to be categorized at least as Type II virtual currencies. This is due to the fact that they can be mutually exchanged with Type I virtual currencies with unspecified persons. The mere fact that there is a soft peg to the US Dollar or other fiat currencies does not make the stable coin a currency denominated asset. The peg serves as a stability mechanism only and does not contain the promise to make a refund in US Dollar or another fiat currency.

Governance tokens which can typically be mutually exchanged with Type I virtual currencies are generally considered Type II virtual currencies.

Stable coins issued under seigniorage models are likely to be classified as virtual currency Type II. Insofar, reference is made to the explanations under item 2.2. above.

Bond and share tokens necessary for the adjustments to the money supply may be classified as securities under the Financial Instruments and Exchange Act (‘FIEA’). The marketing of such securities generally requires registration as Financial Instruments Business Service under the FIEA.

Where bond and share tokens can be mutually exchanged with Type I virtual currencies, they are further deemed Type II virtual currencies.

A listing on one of the registered cryptocurrency exchanges is not possible for securities under the current regulations.

This article only gives a high-level overview of the current regulatory environment for different stable coin models in Japan. Even slight changes to the token design or underlying business model may lead to completely different results. Issuers of stable coins are therefore well advised to consider their model carefully – and in cases where the stable coin is on the market already to assess whether the stable coin can be marketed and eventually listed in Japan.

If you want to learn more or should you need legal or regulatory advice, please feel free to contact us directly under s.saito@innovationlaw.jp.

DISCLAIMER

The stable coins mentioned in this article are used for illustrative purposes only. Given the format of the article not all details of the token design and underlying business model have been considered, so that the results of the assessment may deviate from the results by the regulator or a legal opinion prepared for the respective project. By no means, the explanations should be understood as a legal opinion regarding the stable coins mentioned in this article.

FOOTNOTES

[1] IOU stands for I owe you.

[2] Libra has not gone online yet and only published its whitepaper recently.

[3] According to the terms and conditions of Tether, “the composition of the reserves used to back tether tokens is within the sole control and absolute discretion of Tether” and “may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities”. Tether has not provided audited accounts yet and has repeatedly been accused of market manipulation in the past.

[4] On December 13, 2018, Basis announced that US regulations had a serious negative impact on their ability to launch Basis and forced them to shut down before the project was launched. All funds were returned to their investors.

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Babylon, Bitcoin Staking Mechanism and Japanese Law

Babylon, Bitcoin Staking Mechanism and Japanese Law

Staking/Restaking under Japanese Law

Staking/Restaking under Japanese Law

Crypto Regulations in Japan 2024

Crypto Regulations in Japan 2024

DAO Token Sales under Japanese Laws

DAO Token Sales under Japanese Laws

SEC ICO Warning (Dec 2017)

SEC ICO Warning (Dec 2017)

Initial Coin Offerings (ICO) under Japanese laws

Initial Coin Offerings (ICO) under Japanese laws

Guidance Note on the Japanese Virtual Currency Legislation

Guidance Note on the Japanese Virtual Currency Legislation

New Crypto Regulations of Japan

New Crypto Regulations of Japan

Impacts upon enforcement of the Act concerning Work Style Reform

Impacts upon enforcement of the Act concerning Work Style Reform

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Security Token Offerings in Japan

Security Token Offerings in Japan

Hot wallets, non-custodian exchanges, and smart solutions

Hot wallets, non-custodian exchanges, and smart solutions