Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

There is no legal definition of STOs in Japan. STOs are however commonly understood as the issuance of digital tokens that constitute securities under the applicable laws in order to raise capital.

It should be noted, that the definition of securities varies from jurisdiction to jurisdiction.

For the purposes of this article security tokens are defined as digital tokens that have profit rights attached or which can be redeemed for more than 100 percent of the principal amount in money, virtual currencies or other assets.

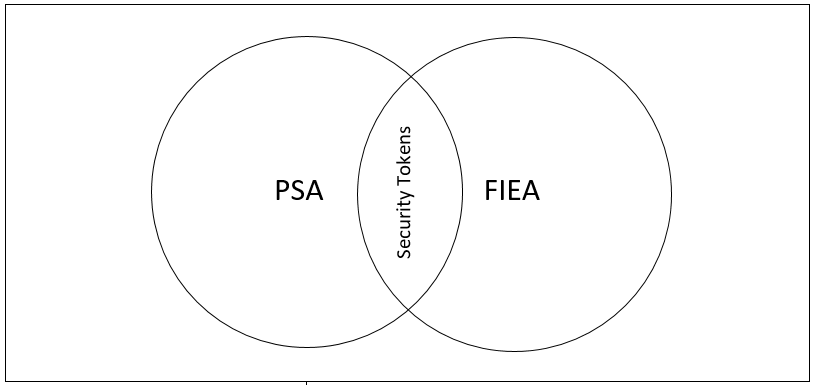

There have not been any public offerings of security tokens in Japan yet. There are cases however, in which companies sold security tokens to qualified institutional investors (QII) in a private placement. We expect increased activities once the amended Payment Services Act (PSA) and Financial Instruments and Exchange Act (FIEA) enter into force.

Under the current framework, STOs fall within the scope of the PSA and FIEA at the same time. As a result, persons involved in an STO must comply with both the PSA and FIEA.

The Financial Services Agency (FSA) interprets the term virtual currency broadly. Tokens issued in an ICO are generally covered.

STOs are considered a type of ICOs. Tokens issued in a STO therefore fall under the PSA as well.

The issuer of tokens must either register as Virtual Currency Exchange Service Provider or sell his tokens through one of the registered exchanges.

Registration is cumbersome and expensive. In the current environment, it is not realistic for token issuers to register as a Virtual Currency Exchange Service Provider.

At the moment it is also not possible to sell tokens through one of the registered exchanges. With the Japan Virtual Currency Exchange Association (JVCEA) publishing draft guidelines on ICOs, this is likely to change in the near future. Provided the guidelines are approved, token issuers will soon be able to sell their tokens via one of the registered exchanges.

Security tokens as defined in this article are explicitly excluded from the JVCEA guidelines.

Under the existing framework, registered exchanges must notify the FSA about the listing of new tokens. The notification has become a de facto approval by the FSA in practice. No tokens have been listed on registered exchanges since late 2017.

Tokens without profit participation rights attached are generally not covered by the FIEA. Security tokens as defined under item 1 above may however be classified as securities under the FIEA. Security tokens that do not represent traditional securities such as shares or bonds may fall under the definition of collective investment schemes (CIS). To be classified as CIS all of the following requirements must be fulfilled:

Cases where tokens are issued in exchange for bitcoin or other cryptocurrencies instead of fiat currencies are not covered at present.

In March this year, the Cabinet submitted a bill revising the PSA and FIEA to the Diet. The Diet approved the bill on 31 May 2019. With the amendments entering into force early next year, the term “virtual currency” will be replaced by the term “crypto assets” and regulations for registered exchanges will be tightened. In addition, Electronically Recorded Transfer Rights as defined in the FIEA will be explicitly excluded from the definition of crypto assets and exclusively be covered by the FIEA.

| Oct 2019 – end 2019 | FSA publishes Cabinet Order as subsidiary legislation and makes it available for public comment. Public comments and final orders will follow two to three months later (end of 2019 to March 2020). |

| ~May 2020 | Amended laws enter into force. |

After the amendments enter into force, most security tokens will exclusively be covered by the FIEA. Only in rare occasions, the PSA might apply at the same time.

The legal term for security tokens under the new FIEA is Electronically Recorded Transfer Right. In order to classify a token as Electronically Recorded Transfer Right a token must fulfill all of the following requirements:

Tokens classified as Electronically Recorded Transfer Right are considered Type I Securities. The implications of such classification are discussed in further detail in the following sections.

In case any of the requirements from (2) to (4) are not fulfilled, a token is considered a type II security. Tokens for which the transferability is technically restricted may fall under the exemption in item (4) above. However, it is unclear at this point, which cases will be covered by the Cabinet Order.

No, tokenized shares or bonds are Type I Securities and not Electronically Recorded Transfer Rights under the FIEA. In practice, this does not make a difference however, since Electronically Recorded Transfer Rights are treated as Type I Securities. As such both are subject to the same disclosure requirements under the FIEA.

Electronically Recorded Transfer Rights are explicitly excluded from the definition of crypto assets under the amended Payment Services Act (PSA). Tokens that do not fall under the definition of Electronically Recorded Transfer Rights due to liquidity constraints may, in theory, be subject to both the PSA and FIEA. It must be noted, however, that in case of liquidity constraints, the token can also not be exchanged with other tokens or fiat currencies. As such, it is unlikely that the token is considered a crypto asset under the PSA.

Electronically Recorded Transfer Rights are considered Type I Securities under the FIEA. As such they are generally subject to disclosure requirements at the time of issuance (e.g. registration documents, prospectus) and subsequently (e.g. quarterly reports, extraordinary reports).

The exact information that must be disclosed at the time of offering will be stipulated by Cabinet Order in the future. In general, the preparation of a prospectus and other disclosure documents takes a considerable amount of time.

Private placements are generally exempted from disclosure requirements.

A public offering is an offering of newly issued Type I securities to at least 50 persons which is not considered a private placement.

The following offers are considered private placements of Type I Securities under the FIEA:

Private placements to QII: Offers to QII with the resale restriction under 5.7 below are considered private placements under the FIEA.

Private placements to specified investors: Offers to specified investors with the resale restriction under 5.7 below are considered private placements under the FIEA. Offers to specified investors other than QII can only be made by financial instruments business operators (FIBO).

Private placements to a small number of investors: Solicitations to less than 50 investors (QII can be excluded from this number) with the resale restriction under 5.7 below are considered private placements under the FIEA.

Private placements to QII: In general securities acquired in a private placement may not be resold to persons other than QII. The exact nature of the restrictions varies depending on the type of securities. In case securities are sold in violation of the restrictions on resale, the issuer must file a registration statement with the FSA.

Private placements to specified investors: In general securities issued in a private placement to specified investors may not be resold to other persons than specified investors. Where securities are sold in violation of these restrictions, the issuer must file a registration statement with the FSA.

Small number of investors: Resale restrictions vary depending on the type of securities. While there are no resale restrictions for shares, restrictions apply to the resale of share options and other securities. In these cases, the securities may only be transferred in bulk. Where the total number of units is less than 50, the units may not be split.

In general, the same restrictions apply. Security tokens are considered “other securities” under the current FIEA Enforcement Order and Cabinet Order to which the same resale restrictions apply in case of private placements. It is possible that additional requirements, such as the implementation of technical measures, will be introduced in the future.

A person engaging in the business of buying and selling security tokens (incl. the provision of intermediary services, public offerings and private placements) must generally register as a FIBO under the FIEA.

There are no restrictions for the self-solicitation of tokens that are classified as traditional type I securities such as stocks. Regulations apply however for the self-solicitation of units in a CIS. Persons offering their own security tokens, which qualify as units in a CIS, must register as type II FIBO even if such units are considered Electronically Recorded Transfer Rights.

Intermediaries in the sale and purchase of security tokens must register as type I FIBO. This applies irrespective of whether the tokens are classified as traditional type I securities or Electronically Recorded Transfer Rights.

Persons intending to operate a security token exchange must obtain a Financial Instrument Market License or the approval as proprietary trading system (PTS), depending on the business model. Since it is difficult to obtain the said license or to registers as PTS, we expect that most of the secondary trading will initially occur OTC.

Under the Japanese Civil Code the transfer of contractual rights generally requires an agreement between the assignor and assignee as well as the consent of the counterparty to the contract. This should be reflected in the contract documentation for the STO.

Electronically Recorded Transfer Rights are not stock or bonds. The provisions on the issuance of stock and bonds under the Companies Act do therefore not apply. If the rights of an anonymous partnership or other funds are tokenized, an approval by the general meeting of shareholders is not necessary. Since the tokenization of an anonymous partnership can be considered an important decision a board resolution is however required.

No, this is not necessary. From a management perspective, it is advisable to issue only tokens that do not harm the rights of existing shareholders.

Listed companies must disclose the issuance of security tokens in a timely manner. What kind

of information must be disclosed should be coordinated with the respective exchange

DISCLAIMER

This article contains a high-level overview and is prepared for general information of our clients and other interested persons. The content has not been confirmed by the relevant authorities, but merely contains information and interpretations that may be reasonably considered in accordance with the applicable laws and regulations. The opinions expressed in this article are our current views and may be subject to change in the future. This article is provided for your convenience only and does not constitute legal advice.

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Babylon, Bitcoin Staking Mechanism and Japanese Law

Babylon, Bitcoin Staking Mechanism and Japanese Law

Staking/Restaking under Japanese Law

Staking/Restaking under Japanese Law

Crypto Regulations in Japan 2024

Crypto Regulations in Japan 2024

DAO Token Sales under Japanese Laws

DAO Token Sales under Japanese Laws

SEC ICO Warning (Dec 2017)

SEC ICO Warning (Dec 2017)

Initial Coin Offerings (ICO) under Japanese laws

Initial Coin Offerings (ICO) under Japanese laws

Guidance Note on the Japanese Virtual Currency Legislation

Guidance Note on the Japanese Virtual Currency Legislation

New Crypto Regulations of Japan

New Crypto Regulations of Japan

Impacts upon enforcement of the Act concerning Work Style Reform

Impacts upon enforcement of the Act concerning Work Style Reform

Stable Coins under Japanese Laws

Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Hot wallets, non-custodian exchanges, and smart solutions

Hot wallets, non-custodian exchanges, and smart solutions