Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

DAO |

FinancialRegulation |

Law |

NFT |

A DAO is a decentralized autonomous organization that drives a business or project forward using smart contracts without a specific owner or manager. Overseas clients sometimes ask our firm whether they can sell DAO tokens in Japan.

| (1) You need to consider Japanese regulations when you sell DAO tokens to Japanese residents, even if you reside outside Japan. (2) Regulations on DAO tokens differ depending on whether they are investment DAO tokens or community DAO tokens. (3) Investment DAO tokens are generally considered “security.” Their sale is usually regulated by the Financial Instrument and Exchange Act (FIEA). The seller must obtain FIEA registration or delegate the sale’s activities to a licensed FIEA company. Some exemptions exist, but they are not easy to use. (4) Sales of community DAO tokens are either (i) unregulated, (ii) regulated by the Crypto Asset Exchange Business Law, or (iii) regulated by the FIEA, depending on the nature of the tokens. |

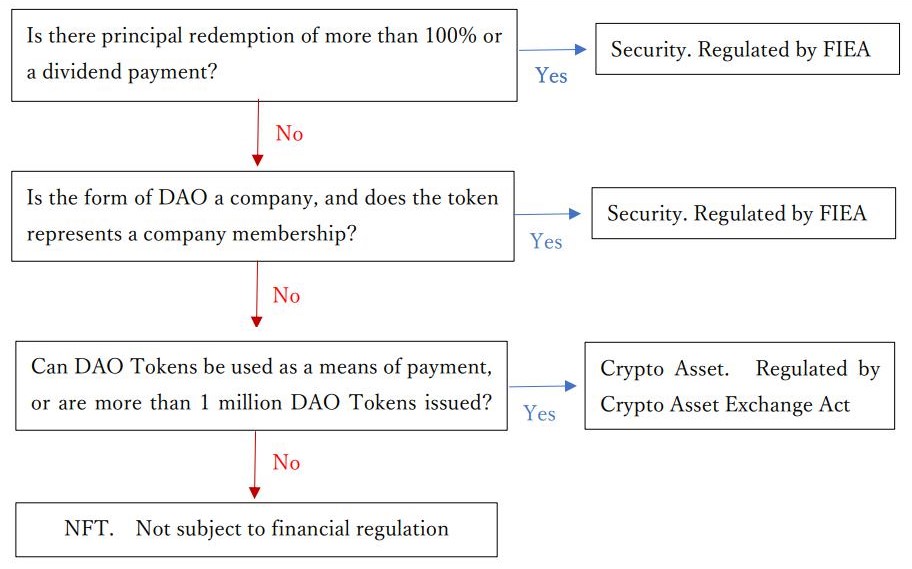

Below is a chart you need to consider before selling DAO tokens to Japanese residents.

<Chart to be considered>

Community DAOs often issue governance tokens.

To consider the financial regulation of sales of DAO tokens in Japan, we must look at (a) whether the DAO provides some kind of dividend or more than 100% redemption of the principal (“Dividend, Etc.”), (b) whether the DAO has any legal entity nature that is similar to a joint stock company or LLC and whether the tokens represent nature similar to shareholders rights, and (c) whether DAO tokens can be used as a payment method.

Tokens in most community DAO do not have any dividend feature or profit distribution feature for token holders. If there are such features, the regulation on investment DAO tokens will be applied. Please see item 4 below.

If a DAO is structured in the form of a company, which happens rarely, and the DAO token awards member rights of the company to token holders, the right might be deemed as securities. Type 1 Financial Instruments Business Registration is required for the sale of those tokens.

In general, many DAOs are formed without clarification of the legal form. Some DAOs just use a smart contract and do not have any form of legal entity. Under Japanese law, such DAOs may be classified as partnerships or “associations without a juridical person.” The rights of partnerships and associations without juridical persons do not fall under securities unless there are Dividend, Etc.

The sale of DAO tokens without Dividend, Etc. and so on issued by an organization other than a company should be classified as a crypto asset or NFT.

If the tokens fall under the definition of crypto asset, their sale shall be made by a licensed crypto asset exchange business operator.

However, if the DAO token is considered an NFT, there are no restrictions on its sale.

In 2023, the Financial Services Agency (FSA) issued guidelines stating the distinction between a crypto asset (FT) and an NFT: (https://www.fsa.go.jp/news/r4/sonota/20221216-2/20221216-2.html).

The guideline states that if the asset does not have “means of payment” characteristics, it is not a crypto asset and that having “means of payment” characteristics can be determined by the following criteria: In general, if (a) DAO tokens cannot be used as a payment method, and (b-1) the price of the token is more than JPY 1,000 or (b-2) the issued number of tokens is less than 1M, the tokens are considered NFTs, and their sale is not regulated.

| FSA’s revised guidelines a) The issuer must make it clear that the tokens are not intended to be used to pay for goods or services to an unspecified person. For, example the terms and conditions provided by the issuer or business operator handling the product clearly prohibit the use of the product as a payment method, or the system is designed to prevent the use of the product as a payment method. b) Taking into consideration the price and quantity of the relevant property value, technical characteristics and specifications, and other factors as a whole, the tokens that can be used to reimburse an unspecified person for the price of the goods and so on must be limited. For example, the tokens must have one of the following characteristics: ・The price per minimum transaction unit must be high enough not to be used as an ordinary means of settlement (JPY 1,000 or more). ・The issued number of tokens divided by the minimum trading unit (issued volume considered after divisibility) must be limited (1 million or less). |

Under the FIEA, DAO tokens that pay Dividend, Etc. generally fall under the category of “electronically recorded transfer rights.” Thus, in order to sell electronically recorded transfer rights, you must either register as a Type 1 Financial Instruments Exchange Business Operator (Type 1 FIEBO) and conduct the sales yourself or have a Type 1 FIEBO do it for you. Furthermore, when soliciting 50 or more persons and issuing 100 million yen or more, the solicitation of the tokens becomes a public offering (Article 2, Paragraph 3 of the FIEA), which requires the submission of complex offering documents and continuous disclosure.

As an exception, if sales are made only to qualified institutional investors (QIIs, professional investors) or wealthy individuals (with financial assets of JPY 100 million or more) who are 49 or younger, and if technical restrictions are in place to prevent other individuals from becoming DAO token holders through resale, then the sale falls under the exception category called “special business for qualified institutions, etc.,” and self-offering only requires a simple notification under Article 63 of FIEA.

We have heard that many investment DAOs in the US are issued to QIIs, and many investment DAOs limit their sales to avoid US security regulations. The problem in Japan is that the definition of “professional investors” is much narrower than in the US. In Japan, one criterion for becoming QII is that corporations and individuals must have at least JPY 1 billion in securities. In the US, a person who has more than USD200,000 annual income can become a QII, and in the EU, a person who has more than EUR500,000 in financial assets (in addition to satisfying other requirements) can be a QII. These requirements are much easier to satisfy than the requirements in Japan.

Japan also has a narrower exception to submit offering documents. In Japan, offering documents are required for offerings exceeding JPY 100 million. In contrast, exemptions apply for offerings less than USD6 million in the US (sales by Reg A Tier 1) and less than EUR5 million in some countries in the EU.

In light of the above, the issuance of investment DAOs is not popular in Japan but is still possible if you obey Japanese regulations.

EOD

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Babylon, Bitcoin Staking Mechanism and Japanese Law

Babylon, Bitcoin Staking Mechanism and Japanese Law

Staking/Restaking under Japanese Law

Staking/Restaking under Japanese Law

Crypto Regulations in Japan 2024

Crypto Regulations in Japan 2024

SEC ICO Warning (Dec 2017)

SEC ICO Warning (Dec 2017)

Initial Coin Offerings (ICO) under Japanese laws

Initial Coin Offerings (ICO) under Japanese laws

Guidance Note on the Japanese Virtual Currency Legislation

Guidance Note on the Japanese Virtual Currency Legislation

New Crypto Regulations of Japan

New Crypto Regulations of Japan

Impacts upon enforcement of the Act concerning Work Style Reform

Impacts upon enforcement of the Act concerning Work Style Reform

Stable Coins under Japanese Laws

Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Security Token Offerings in Japan

Security Token Offerings in Japan