Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

cryptographic assets |

DeFi |

Japanese law |

LIDO |

liquid staking |

staking |

This article describes the structure of and applicable Japanese law to liquid staking, which has been expanding rapidly in recent years, and its most significant protocol, LIDO.

| (1) To analyze liquid staking, it is generally necessary to consider (1) the sales, purchase, and exchange regulations of the Payment Services Act (We call crypto regulation in the Payment Services Act the “Crypto Assets Act” after this), (2) the custody regulations of the Crypto Assets Act, and (3) the fund regulations of the Financial Instruments and Exchange Act, which is a kind of Japanese Security Act (the “FIEA”). (2) For staking, LIDO accepts staking of ETH and issues stETH in exchange for staked ETH. We believe that this conduct is not considered as “sales, purchase, or exchange of crypto asset” in the terms of the Crypto Assets Act. We believe stETH is just issued as proof of staking and not “exchange” under the Japanese Civil Code. (3) If the staking of ETH is considered a custody of crypto assets, the custody regulation of the Crypto Assets Act may apply. However, if the deposit is made against a smart contract and the protocol or node operator is technically incapable of transferring the ETH, etc., the custody regulation does not apply. (4) The most controversial question should be whether the fund regulations of the FIEA would apply to liquid staking. LIDO’s mechanism might be considered as a fund because (i) ETH, etc., is contributed to the protocol by a user of LIDO, (ii) the node operator manages it, (iii) a portion of the staking fee is distributed to the user, (iv) the user seems to bear the penalty risk and thrashing risk of the staking, and (v) this mechanism seems to like a fund. However, we believe that we can argue that the fund regulation will not apply to LIDO because (i) staked ETH itself is not converted to anything, (ii) it is used for just a kind of collateral to compensation to penalty/slashing, and (iii)we can argue this mechanism is entirely different from usual funds. (5) In addition to the above, we can argue that the Japanese financial regulation might not apply to DeFi if there is no “operator” because Japanese law just regulates persons and legal persons. However, this argument needs an actual fact analysis of the relevant liquid staking. Further, this argument cannot apply to a person or legal entity, if any, who intermediate Japanese residents to DeFi. Thus, the arguments from (1) to (4) above are important. |

Liquid staking is a DeFi (decentralized finance) mechanism whereby a person receives a staking fee for a crypto asset while receiving an additional alternative asset (a staking-proof token) and can invest said alternative asset in another DeFi.

Proof of Stake (POS) is the authentication mechanism of the blockchain by a person who has a certain level of involvement (stake) in the crypto asset.

Unlike the Proof of Work (POW) mechanism used in Bitcoin and other cryptocurrencies, authentication can be performed without requiring a large amount of calculations, thus reducing electricity consumption and making it more environmentally friendly.

Ethereum has been structured using POS instead of POW from ETH 2.0. In Ethereum staking, (1) you can become a validator by depositing 32 ETH, (2) the validator authenticates each transaction on Ethereum and thereby receives a certain amount of ETH as a reward, and (3) if the validator intentionally provides false information, he/she will be penalized by forfeiting a part of the deposited ETH (thrashing), (4) a validator is always required to be online, and if they are down, they will also be penalized to a certain extent.

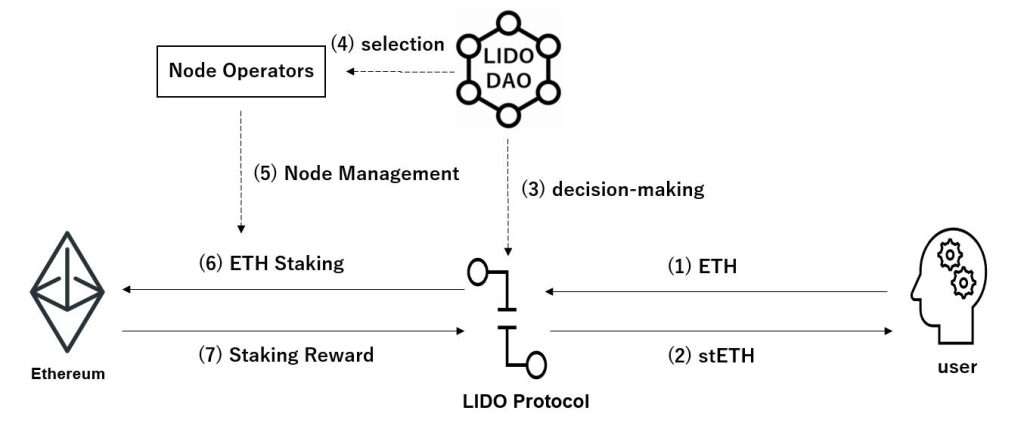

LIDO is the world’s largest protocol for Liquid Staking. At present, it is estimated that more than 30% of the staking volume of Ethereum is done via LIDO. LIDO is supposed to work as follows:1

Prepared by So&Sato Law Offices from published materials

①LIDO allows users to stake ETH without maintaining their staking infrastructure and without economically locking up their assets.

②When a user wants to stake ETH to LIDO, the user should send ETH to LIDO’s smart contract. In response, the user receives a 1:1 token called stETH.

③stETH is a token that represents the deposit of ETH to LIDO for staking, and when a user sends stETH to LIDO to burn stETH, the user will receive ETH. stETH can be freely bought and sold, and if there is another DeFi that accepts stETH, the user can earn double rewards by using stETH on another DeFi (however, DeFi protocols that accept stETH still seem to be limited).

④LIDO will use ETH received through the smart contract to perform staking. LIDO will receive 10% of the reward obtained from staking, which will be distributed to the person in charge of the staking (node operator) and the LIDO DAO. The remaining 90% will be distributed to the users. The distribution to the users is made by adding the number of stETH in the address of stETH, and the number of ETH managed by LIDO is always the same as the number of stETH.

⑤LIDO uses multiple node operators. Node operator candidates apply to LIDO, stating that they wish to become node operators, their experience and technical capabilities, etc., and are then voted on by the DAO, which is composed of LIDO token holders, the LIDO’s governance tokens, to determine whether they are eligible to become node operators.

⑥Note that ETH has thrashing risks and penalties. LIDO hedges against such risks by using a large number of node operators. LIDO also manages some ETH separately and uses it as insurance against thrashing risk.

⑦LIDO is an open-source, peer-to-peer protocol and is not operated by a single operator, etc., as the LIDO DAO makes the decision on its operation.

When offering liquid staking like LIDO, it is necessary to consider whether the trading and custody regulations of the Crypto Assets Act apply and whether the fund regulations of the FIEA apply.

When a user contributes ETH to LIDO, the user will receive stETH, and conversely, when a user sends stETH to LIDO, the user will receive ETH.

The question arises as to whether this action constitutes an exchange of ETH for stETH. If it is considered an exchange of crypto assets, the regulations of the crypto asset exchange services might apply.

StETH, however, is issued to prove the deposit of ETH, and we believe the issuance of such stETH does not constitute a sale or exchange under civil law and thus does not constitute an exchange of crypto assets (and vice versa).

The contribution of ETH to LIDO might be considered a deposit of crypto assets to LIDO and raises the issue of whether the custody regulations of the Crypto Assets Act apply to LIDO.

However, it appears that the contribution to LIDO is a contribution to a smart contract, and LIDO cannot use said ETH except for staking (i.e., it does not control the private key) due to the structure of the smart contract.

Under the Japanese custody regulations, “If a business operator does not possess any of the private keys necessary to transfer the crypto assets of a user, the business operator is not considered to be in a position to proactively transfer the crypto assets of the user. In such case, the business operator is basically not considered to fall under the category of “managing crypto assets for others” as defined in Article 2.7.4 of the Payment Services Act. (Result of Public Comment No. 9 on the Draft Cabinet Order and Cabinet Office Ordinance Concerning Amendment to the Payment Services Act, etc. of 2019). If the smart contracts can technically prevent the free transfer of ETH by people related to LIDO, we believe LIDO is not considered to be subject to the custody regulations under the Crypto Assets Act.

The question arises whether LIDO or liquid staking is considered a fund (collective investment scheme), given the mechanism of receiving ETH contributions, the node operator managing it, distributing a portion of staking fees to users, and users bearing the risk of thrashing and other penalty risks.

The definition of a fund under Japanese law is generally as follows (Article 2, Paragraph 2, Items 5 and 6 of the FIEA). If a fund investor’s right is tokenized, the tokens are considered electronically recorded transferable rights (Article 2, Paragraph 3, Pillar 1 of the same law).

If the issuer itself is offering or private offering the tokens, registration as a Type 2 Financial Instruments Business is required (Article 2, Paragraph 8, Item 7, (g), Article 28, Paragraph 2, Item 1, and Article 29 of the same law, Article 1-9-2, Item 2 of the Order for Enforcement of the FIEA), and if the third party is offering or private offering the tokens, registration as a Type 1 Financial Instruments Business is required (Article 28, Paragraph 1, Item 1 and Article 29 of the FIEA).

| Definition of the Funds under Japanese law (A) (i) partnership contracts, (ii) silent partnership agreements, (iii) limited partnership agreements for investment, (iv) limited liability partnership agreements, (v) membership rights in incorporated associations, and (vi) other rights (excluding those under foreign laws and regulations). (B) The Investor(s) receives the right to receive dividends of income or distribution of properties that arise from a business conducted by using money (including crypto assets) invested or contributed by the investor(s). (C) None of the following (a) the case where all of the investors are involved in the business subject to the investment (in the way specified by a Cabinet Order) (b) the case where the investor(s) shall not receive dividends or principal redemption more than their investment Funds under Foreign Law (D) Rights under foreign laws that are similar to the above rights. |

The concept of “other rights” in (A) above is very broad, and it is said that (i) through (v) are merely an enumeration of examples, regardless of the legal form. It can be argued that tokens issued in fully decentralized finance are not “rights” because they are not considered “rights” in the usual legal interpretation, but there is currently a prevailing view that some rights are recognized for Bitcoin, etc.2, and in relation to this article, we assume that some kind of right is recognized even for smart contracts.

Nor does it fall under any of the exceptions in (C) above.

The main issue is the interpretation of (B) above, which states “dividends of income or distribution of properties that arise from a business conducted by using money” and “invested or contributed.” If we simply take the point that ETH is sent to the smart contract, it is used in the business of the POS, and the award from staking ETH is distributed to users, it would seem to satisfy both the “dividends of income or distribution of properties that arise from a business conducted by using money,” and “invested or contributed” requirement.

However, liquid staking is very different from ordinary funds in the following respects, and, arguably, liquid staking is not a fund to which the FIEA applies.

(1)In the case of a regular fund, the money and other assets contributed are fully owned by the fund operator, and the fund operator can technically use them in various ways, although they are contractually bound. In the case of liquid staking, the ETH contribution is made to the smart contract, and LIDO or node operators are not free to use it; ownership (ownership-like rights) over ETH is always considered to be held by the user,

(2)In the case of a regular fund, the money received is used to purchase shares, fund a business, etc., and changes from money to shares, etc. In LIDO staking, the ETH sent to the smart contract is not specifically changed into anything else but is maintained as it is.

(3)The only reason ETH is locked is to ensure that there is no thrashing in the event of fraudulent reporting in the validation process or penalties if a node goes offline.

(4)Based on (1) through (3) above, if we compare the legal nature of staking to a traditional economic act, it can be thought that the user is merely locking ETH into a smart contract as a kind of collateral to secure default liability and is merely receiving compensation for providing third party collateral. The provision of such collateral and the receipt of compensation do not satisfy the requirements of “dividends of income or distribution of properties that arise from a business conducted by using money” and “invested or contributed,” as referred to in the fund.

In the case of DeFi, it could be argued that the operator does not exist in the first place and is not subject to regulation. Japanese law is a legal system that regulates persons and legal entities, such as operators. A completely decentralized financing scheme would not be subject to regulation. However, we need to carefully consider whether there really is no operator for DeFi. In general, DeFi aims for the operator to be non-existent, but even so, it is unclear whether many DeFi are truly completely operatorless.

Further, if the scheme is subject to financial regulations under the law, assuming there is an operator, the intermediary for the scheme could be subject to regulations even if there is no operator for DeFi itself. It would prevent, for example, an unlicensed Japanese company from sending customers to the DeFi.

Therefore, when examining the legal issues of DeFi, it is necessary to consider two issues: (i) if there is an operator, whether it is subject to legal regulation, and (ii) whether an operator exists.

However, it is unclear from the published documents whether the LIDO DAO is truly decentralized, so this article mainly discusses (i) above.

Disclaimer

The content of this article has not been confirmed by the relevant authorities or organizations mentioned in the article but merely reflects a reasonable interpretation of their statements. The interpretation of the laws and regulations reflects our current understanding and may, therefore, change in the future. This article does not recommend the investment in LIDO or liquid staking. This article provides merely a summary for discussion purposes. If you need legal advice on a specific topic, please feel free to contact us.

Is the Android ‘Me’ the Same Person?- Future Legal Systems Contemplated at Osaka Kansai Expo 2025

Babylon, Bitcoin Staking Mechanism and Japanese Law

Babylon, Bitcoin Staking Mechanism and Japanese Law

Staking/Restaking under Japanese Law

Staking/Restaking under Japanese Law

Crypto Regulations in Japan 2024

Crypto Regulations in Japan 2024

DAO Token Sales under Japanese Laws

DAO Token Sales under Japanese Laws

SEC ICO Warning (Dec 2017)

SEC ICO Warning (Dec 2017)

Initial Coin Offerings (ICO) under Japanese laws

Initial Coin Offerings (ICO) under Japanese laws

Guidance Note on the Japanese Virtual Currency Legislation

Guidance Note on the Japanese Virtual Currency Legislation

New Crypto Regulations of Japan

New Crypto Regulations of Japan

Impacts upon enforcement of the Act concerning Work Style Reform

Impacts upon enforcement of the Act concerning Work Style Reform

Stable Coins under Japanese Laws

Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Libra, Maker’s Dai and other Stable Coins under Japanese Laws

Security Token Offerings in Japan

Security Token Offerings in Japan