Japan has enacted and improved crypto regulations since 2017. Japan was once one of the most crypto-friendly nations in the world, but after 2018, it adopted a stricter regulatory stance. It is, however, now becoming more friendly to the Web3 industry again, with an intention to attract foreign investment.

This article provides an overview of cryptoasset regulations in Japan in 2024.

History of Cryptoasset Regulations in Japan

| Early Friendly Era | |

| February 2014 | MtGox, located in Shibuya, Tokyo, and the largest exchange in the world, went bankrupt. |

| March 2014 | Japanese LDP (Liberal Democratic Party, a governing party in Japan) discussed with the government and decided not to regulate virtual currency at that stage but asked the industry to form a self-regulatory organization. |

| May 2016 | Japan enacted the first virtual currency act in the world. The act was made as an amendment to the Payment Service Act (“PSA”). The act was friendly to startups and intended to foster the industry. |

| April 2017 | The amended PSA stated above was enforced. |

| 2017 | There were ICO booms all over the world, and the price of crypto went up. The trading volume of Japanese exchanges became number 1 in the world. Many foreign players came to Japan to start their business. |

| Era of Stricter Regulation | |

| February 2018 | A massive hacking incident, under which approximately JPY 58 billion equivalent NEM was hacked, happened in Japan (Coincheck incident). |

| 2018-2021 | After the Coincheck incident, the Japanese government tightened the operation of the regulation. Many exchanges received business improvement orders and suspension orders, and the market became shrunk. |

| May 2020 | The amended PSA and the amended FIEA were enforced. |

| Era that Web3 became a national strategy | |

| 2021- | The Japanese government’s national growth strategy in 2021 includes the statement that Web3 became one of the national strategies. Under this strategy, the LDP’s Web3 project team has issued policy recommendations titled the Web3 White Paper1in order to foster Web3 every year since 2022. |

| June 2022 | Japan enacted one of the world’s earliest stablecoin regulations. The act was made as an amendment of the PSA and the Banking Act. |

| 2022 | In 2002, there were collapses of Tera Luna, Three Arrows Capital, and the FTX Group. As a result, the global regulatory environment became stricter. However, Japan had already implemented stringent regulations, which proved effective. (*1) Therefore, Japan did not need to change its regulations even after these collapses.

(*1) Even in the FTX Group’s bankruptcy, the assets of FTX Japan’s customers were all preserved because the regulations required 100% of users’ assets to be segregated. |

| June 2023 | Stablecoin regulation was enforced. |

| May 2024 | DMM Bitcoin was hacked, resulting in a loss of approximately JPY 48.2 billion worth of Bitcoin. However, we have not seen any regulatory tightening in response to this incident at this stage. |

The PSA defines cryptoassets as property value with the following elements:

| (i) which is recorded by electronic means and can be transferred by using an electronic data processing system, (ii) which can be used in relation to unspecified persons for the purpose of paying consideration for the purchase or leasing of goods, etc. or the receipt of provision of services and can also be purchased from and sold to unspecified persons acting as counterparties, and (iii) excluding the Japanese currency, foreign currencies, currency-denominated assets, and Electronic Payment Instruments. |

Under the PSA, the Cryptoasset Exchange Service means any of the following acts carried out in the course of trade:

| (i) sale and purchase of cryptoassets (i.e., exchange between cryptoassets and fiat currency) or exchange of cryptoassets into other cryptoassets; (ii) intermediary, brokerage, or agency service for the acts described above (i); (iii) management (custody) of fiat currency on behalf of the users/recipients in relation to the acts described above in (i) and (ii) and (iv) management (custody) of cryptoassets on behalf of the users/recipients. |

Sales and purchases of cryptoassets to Japanese residents are not subject to the regulation unless they are conducted “in the course of trade (gyo to shite)”. An act in the course of trade is generally understood to be a repetitive and continuous act vis-à-vis the public. For example, trading in cryptoassets for one’s own investment purposes or taking custody of cryptoassets of a wholly owned subsidiary are not considered acts in the course of trade.

It should be noted that just because your clients are only institutional investors is not considered as it is not in the course of trade.

Whether or not a CESP solicits Japanese residents is also considered an important factor in determining the regulation’s application. The determination of whether solicitation towards residents of Japan is being conducted is made on a case-by-case basis. For instance, actions such as not blocking access to a website from Japan, providing information in Japanese, or introducing products at events in Japan could be considered factors that indicate solicitation towards residents of Japan.

The custodian of cryptoassets shall take the CESP license. According to the FSA guidelines, whether each service constitutes the management of cryptoassets should be determined based on its actual circumstances. Generally, if a service provider can technically transfer its users’ cryptoassets, it falls under the category of the management of cryptoassets. If a service provider does not possess any of the private keys necessary to transfer its users’ cryptoassets, the service provider is basically not considered to manage cryptoassets.

Accordingly, wallet services, such as non-custodial wallets, where the users manage the private key on their own, are not considered to constitute the management of cryptoassets.

An intermediary generally means a factual act that involves efforts to conclude a legal act between two others. Brokerage or agency service means to perform a legal act in one’s own name and for the account or on behalf of another person.

With respect to a purchase and sale agreement of cryptoassets between third parties, the acts of (i) soliciting the signing of the agreement, (ii)explaining the product for the purpose of solicitation, and (iii) negotiating the terms and conditions fall, in principle, under the category of an intermediary.

The mere distribution of product information papers, etc., may not fall under the category of an intermediary and should be considered on a case-by-case basis.

The PSA requires minimum capital, financial requirements, a physical office, a sufficient number of personnel on staff, segregation of assets, an annual audit, a customer identity verification system, accountability to users, protection of person/s’ information, including sensitive information, and, if outsourced, must retain authority. The service provider must be equipped with the systems for adequate operation and legal compliance deemed necessary to operate a Cryptoasset Exchange Service appropriately and securely. Although the applicant must have a minimum capital base of at least JPY 10 million, and it must not be in negative assets, from our experience, the cost of obtaining the license and starting the internet exchange business can be more than JPY 1 billion.

We are often asked by companies interested in entering the Japanese crypto market whether they can start their business by acquiring an already licensed CESP rather than obtaining a new license. The answer is Yes. Regulatory speaking, change of major shareholders is done just ex-post notification and you can start your business after purchasing the already licensed CESP.

The major issue here is that the purchased CESP shall satisfy the governance and compliance levels, which are similar to those a new licensed exchange shall achieve. If one purchases a cheap CESP, which is just having a license but has not done a business actively, to reach these levels might be difficult and time-consuming. Furthermore, if you wish to change the business model or system of the purchased CESP, you must provide an explanation to and obtain approval from the FSA. The cost of purchasing the licensed CESP, combined with this additional expense, can sometimes be comparable to the cost of obtaining a new license. Therefore, careful consideration is necessary.

The PSA requires the users’ cryptoassets to be segregated from the CESP. Further, the CESP shall keep (i) at least 95% of the users’ cryptoassets in cold wallets and (ii) equivalent to 100% minus those kept in the left column of its own cryptoassets in cold wallets. Thus, as a consequence, the CESP shall hold the equivalent of 100% of users’ cryptoassets in cold wallets.

With respect to fiat currency, the CESP shall deposit its users’ fiat currency in a bank account under a different name from where the CESP deposits its own funds.

A CESP must undergo an annual audit of its financial statements and segregation of assets.

Anti Money Laundering law requires CESPs to conduct a know-your-customer of users. Stricter regulations for anti-money laundering came into effect on June 1, 2023. According to the new Travel Rules, when assets over a certain amount are sent by a user, the receiving and sending CESPs must share information about the users. The lack of interoperability in such information-sharing systems has prevented users from sending and receiving cryptoassets between some CESPs.

The regulations applicable to decentralized exchanges (DEX) are not clear. There is an argument that the regulations do not apply to exchanges that are completely decentralized and have no administrator at all, as there is no entity subject to crypto regulations. However, it is necessary to carefully consider whether there is truly no administrator. Further, entities that provide access software to a DEX may be subject to the regulations for being intermediaries.

As stated later in section III. 1, the sale of cryptoassets issued by oneself is subject to crypto regulations. Providing liquidity to a DEX for cryptoassets issued by oneself may also be considered as engaging in the sales of the cryptoassets.

Pure NFTs, such as trading cards and in-game items recorded on blockchains that do not function as payment instruments, are not considered cryptoassets. The FSA states that the distinction between cryptoassets and pure NFTs is as follows:

(i) the issuer of the NFTs prohibits its use as a payment instrument by technical feature or by agreement

(ii) the quantity and price of the NFTs are not suitable as a payment instrument (specifically, one NFT costs more than ¥1,000 or the total number of the NFTs issued is less than 1 million).

Generally speaking, pure NFTs are not regulated in Japan. Please, however, note that whether NFTs are considered as “pure” NFTs needs careful discussion. For example, if an NFT gives some dividend or economic benefit, it might be considered as a security. Further, an NFT, which is linked to real-world assets, might require a discussion of whether regulation of real assets may apply.

Japan was one of the first countries in the world to establish stablecoin regulations. Stablecoins pegged to fiat currency are defined as electronic payment instruments and require a license different from CESP to offer the related service.

Other stablecoins that adjust their value through algorithms could be regulated as cryptoassets or securities. Stablecoins classified as cryptoassets are subject to crypto regulations, while stablecoins classified as securities are subject to securities regulations (FIEA).

ICO (Initial Coin Offering) is an act of issuing and selling tokens to raise fiat currency or crypto assets from the public. ICO is regulated in Japan. The applicable regulations depend on the legal nature of the issued tokens. If the tokens are considered securities, the token issuance will be regulated by the FIEA. If the tokens are considered cryptoassets, the token issuance will be regulated by the PSA.

The issuance of new cryptoasset-type tokens in Japan is generally done by IEO (Initial Exchange Offering). IEO is an act of raising fiat currency or cryptoassets by an entity entrusting the sales of tokens to a licensed CESP. In the case of IEO, if the issuer itself does not conduct sales activity, the issuer does not need to take the crypto exchange license. If, however, the issuer itself wants to conduct sales activity for its new tokens, it needs to have a crypto exchange license, which requires significant cost and time compared to IEO. Several IEO projects have already been launched in Japan.

The IEO process requires examinations by the exchange, JVCEA, a Japanese self-regulatory organization, and the FSA. The examination checks the feasibility of the project for which the funds will be used, the financial soundness of the issuer, and other factors.

SAFT (Simple Agreement for Future Tokens) is a way to raise funds in exchange for the right to purchase tokens to be issued in the future. SFAT targeting Japanese residents is considered to be subject to fund regulation or crypto regulation, depending on the legal nature of the agreement. However, both regulations do not apply unless the act is done in the course of trade, so we may argue that entering into a SAFT with limited numbers of specific persons, such as business partners who will contribute to developing projects, should not be regulated.

SAFE (Simple Agreement for Future Equity) with token warrant is subject to general equity investment regulations, depending on the attributes of involved entities and investors.

Japanese entities sometimes use J-KISS, a Japanese convertible equity, with a side letter that provides tokens.

Generally speaking, we believe staking service for POS tokens is not regulated in Japan. For example, staking one’s own cryptoassets or becoming a validator for ETH is not regulated in Japan.

Not all staking services, however, are exempted from the regulation. If service providers manage the private keys of users’ cryptoassets (we understand some exchanges provide those services), custody regulation may apply. In addition to managing private keys, if the service providers distribute rewards as well as slashing penalties to the users, fund regulations might apply.

We understand that there are some NFT projects that say that they sell NFTs for crypto, and purchasers can stake NFTs, and can get rewards. We understand fund regulation might apply to such cases, especially in cases where staking does not have any actual usage for providing security.

In crypto lending services, a service provider borrows cryptoassets from users for a certain period of time and pays a lending fee in exchange. No regulation applies to that lending because the Money Lending Business Act regulates money lending, but it does not deem cryptoassets as money.2

It should be noted that crypto custody regulations may apply in cases where the service is considered as custody, not lending, even if a service is titled as crypto lending. One factor that distinguishes lending and custody is whether users can withdraw their assets at any time (deposit) or whether there is a specific required time of non-withdrawal (lending).

Mining cryptoassets requires large amounts of electricity. Thus, mining appears to be regulated in some countries, such as Kazakhstan3Regulation of mining in certain areas in Russia is also being discussed4. In Japan, mining itself is not regulated.

A business that collects money from the public to conduct mining operations and then distributes the proceeds from mining to the customers may be regulated under the FIEA as a fund.

Schemes that one sell mining machines, accept deposits of the machines, and promise to pay fees for the mining results may also be regulated under the Act on Deposit Transactions. If the Act on Deposit Transactions is applied, the business must obtain confirmation from the Prime Minister, but it is said that to get such confirmation is nearly impossible. Creating a scheme to avoid such regulation is important.

principle, classified as miscellaneous income. Miscellaneous income is income that is neither interest income, dividend income, real estate income, business income, employment income, retirement income, forestry income, transfer income, or temporary income. The tax rate for miscellaneous income ranges from 5% to 45%, depending on the amount of total income. The maximum tax rate is about 55% when we calculate income tax as well as residential tax and special reconstruction income tax.

Profit generated by cryptoassets transactions is subject to corporate tax which is about 30% depending on the amount of income and how big a company is.

Cryptoassets for which there is an active market must be valued using the mark-to-market method at the end of the fiscal year and are taxable even if companies do not sell them.

This unrealized gain tax treatment became a huge issue in Japan, and many Web3 companies left Japan.

In 2022, the Japanese government decided to reform this unrealized gain tax, and now the tax is not levied if an issuing company of tokens continues to hold its tokens with certain technical transfer restrictions.

In 2023, another tax reform was proposed and approved by the government. Under the reform, an unrealized gain tax is not applied if a company holds tokens with a certain transfer restriction, even in the case that tokens are issued by other entities (including Bitcoin and Ether etc.)

Disclaimer

The content of this article has not been verified by the relevant authorities or organizations mentioned herein and represents only a reasonable interpretation of their statements. Our interpretation of laws and regulations reflects our current understanding and may change in the future. This article is not intended to be legal advice and provides a summary for discussion purposes only. If you need legal advice on a specific topic, please feel free to contact us.

EOD

A DAO is a decentralized autonomous organization that drives a business or project forward using smart contracts without a specific owner or manager. Overseas clients sometimes ask our firm whether they can sell DAO tokens in Japan.

| (1) You need to consider Japanese regulations when you sell DAO tokens to Japanese residents, even if you reside outside Japan. (2) Regulations on DAO tokens differ depending on whether they are investment DAO tokens or community DAO tokens. (3) Investment DAO tokens are generally considered “security.” Their sale is usually regulated by the Financial Instrument and Exchange Act (FIEA). The seller must obtain FIEA registration or delegate the sale’s activities to a licensed FIEA company. Some exemptions exist, but they are not easy to use. (4) Sales of community DAO tokens are either (i) unregulated, (ii) regulated by the Crypto Asset Exchange Business Law, or (iii) regulated by the FIEA, depending on the nature of the tokens. |

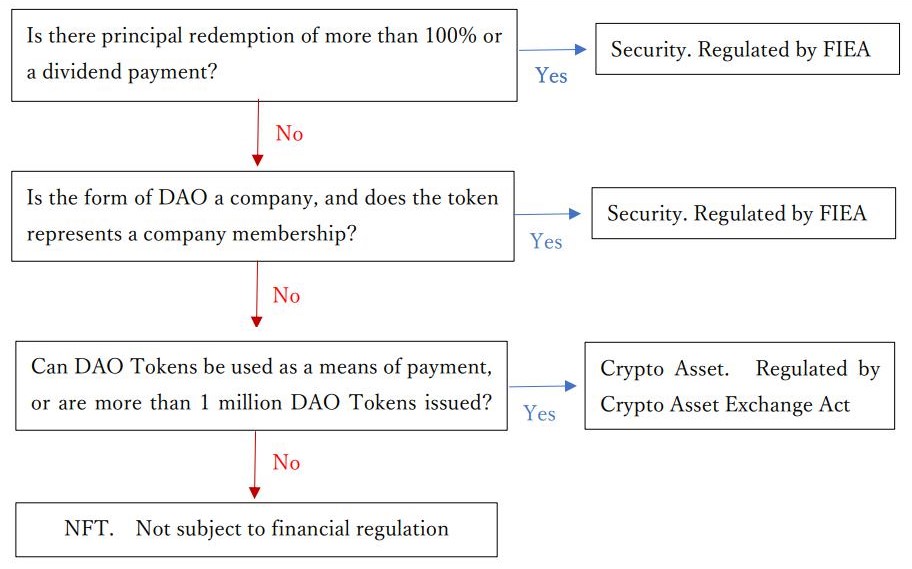

Below is a chart you need to consider before selling DAO tokens to Japanese residents.

<Chart to be considered>

Community DAOs often issue governance tokens.

To consider the financial regulation of sales of DAO tokens in Japan, we must look at (a) whether the DAO provides some kind of dividend or more than 100% redemption of the principal (“Dividend, Etc.”), (b) whether the DAO has any legal entity nature that is similar to a joint stock company or LLC and whether the tokens represent nature similar to shareholders rights, and (c) whether DAO tokens can be used as a payment method.

Tokens in most community DAO do not have any dividend feature or profit distribution feature for token holders. If there are such features, the regulation on investment DAO tokens will be applied. Please see item 4 below.

If a DAO is structured in the form of a company, which happens rarely, and the DAO token awards member rights of the company to token holders, the right might be deemed as securities. Type 1 Financial Instruments Business Registration is required for the sale of those tokens.

In general, many DAOs are formed without clarification of the legal form. Some DAOs just use a smart contract and do not have any form of legal entity. Under Japanese law, such DAOs may be classified as partnerships or “associations without a juridical person.” The rights of partnerships and associations without juridical persons do not fall under securities unless there are Dividend, Etc.

The sale of DAO tokens without Dividend, Etc. and so on issued by an organization other than a company should be classified as a crypto asset or NFT.

If the tokens fall under the definition of crypto asset, their sale shall be made by a licensed crypto asset exchange business operator.

However, if the DAO token is considered an NFT, there are no restrictions on its sale.

In 2023, the Financial Services Agency (FSA) issued guidelines stating the distinction between a crypto asset (FT) and an NFT: (https://www.fsa.go.jp/news/r4/sonota/20221216-2/20221216-2.html).

The guideline states that if the asset does not have “means of payment” characteristics, it is not a crypto asset and that having “means of payment” characteristics can be determined by the following criteria: In general, if (a) DAO tokens cannot be used as a payment method, and (b-1) the price of the token is more than JPY 1,000 or (b-2) the issued number of tokens is less than 1M, the tokens are considered NFTs, and their sale is not regulated.

| FSA’s revised guidelines a) The issuer must make it clear that the tokens are not intended to be used to pay for goods or services to an unspecified person. For, example the terms and conditions provided by the issuer or business operator handling the product clearly prohibit the use of the product as a payment method, or the system is designed to prevent the use of the product as a payment method. b) Taking into consideration the price and quantity of the relevant property value, technical characteristics and specifications, and other factors as a whole, the tokens that can be used to reimburse an unspecified person for the price of the goods and so on must be limited. For example, the tokens must have one of the following characteristics: ・The price per minimum transaction unit must be high enough not to be used as an ordinary means of settlement (JPY 1,000 or more). ・The issued number of tokens divided by the minimum trading unit (issued volume considered after divisibility) must be limited (1 million or less). |

Under the FIEA, DAO tokens that pay Dividend, Etc. generally fall under the category of “electronically recorded transfer rights.” Thus, in order to sell electronically recorded transfer rights, you must either register as a Type 1 Financial Instruments Exchange Business Operator (Type 1 FIEBO) and conduct the sales yourself or have a Type 1 FIEBO do it for you. Furthermore, when soliciting 50 or more persons and issuing 100 million yen or more, the solicitation of the tokens becomes a public offering (Article 2, Paragraph 3 of the FIEA), which requires the submission of complex offering documents and continuous disclosure.

As an exception, if sales are made only to qualified institutional investors (QIIs, professional investors) or wealthy individuals (with financial assets of JPY 100 million or more) who are 49 or younger, and if technical restrictions are in place to prevent other individuals from becoming DAO token holders through resale, then the sale falls under the exception category called “special business for qualified institutions, etc.,” and self-offering only requires a simple notification under Article 63 of FIEA.

We have heard that many investment DAOs in the US are issued to QIIs, and many investment DAOs limit their sales to avoid US security regulations. The problem in Japan is that the definition of “professional investors” is much narrower than in the US. In Japan, one criterion for becoming QII is that corporations and individuals must have at least JPY 1 billion in securities. In the US, a person who has more than USD200,000 annual income can become a QII, and in the EU, a person who has more than EUR500,000 in financial assets (in addition to satisfying other requirements) can be a QII. These requirements are much easier to satisfy than the requirements in Japan.

Japan also has a narrower exception to submit offering documents. In Japan, offering documents are required for offerings exceeding JPY 100 million. In contrast, exemptions apply for offerings less than USD6 million in the US (sales by Reg A Tier 1) and less than EUR5 million in some countries in the EU.

In light of the above, the issuance of investment DAOs is not popular in Japan but is still possible if you obey Japanese regulations.

EOD

A blockchain game is a game that uses the blockchain and uses crypto assets, tokens or NFTs (Non-Fungible Tokens).

In a typical game the following occurs:

(1) user purchases game assets that belongs to the game operator rather than the user,

(2) such game assets cannot be freely transferred, sold, or lent out, and

(3) even time-consuming data disappears after game distribution ends.

Whereas in blockchain games, it is said that the following occurs:

(1) the user is the holder of the token (game asset),

(2) the token can be transferred, sold, or lent out to third parties,

(3) third parties can also use the token, and

(4) as long as the blockchain exists,5the recorded digital assets will exist in perpetuity.

When providing a blockchain game to Japanese residents, the laws listed below should be taken into account. Here is a summary of the laws that pertains to this matter:

| (1) Fund Settlement Law and Security Act |

| To issue and sell NFT itself is not regulated in Japan. Exception to it is (i) if tokens are deemed as crypto assets, such as fungible token which might be used as a payment method, they might be regulated under the Fund Settlement Law and (ii) if tokens are deemed as security, such as tokens including dividend feature, they might be regulated by the Financial Instrument Exchange Act. |

| (2) Act against Unjustifiable Premiums and Misleading Representations (hereinafter refer to Premiums Law or Premium and Representation Law) |

| Blockchain Game players might be given tokens, digital currencies, NFTs, digital assets or other gifts which have financial value when a user register, login, play a blockchain game. These gifts might be considered “premiums” or “free gifts” under the Premiums Regulations of the Premiums Law and the value of them are limited. |

| If the Play to Earn games allow players to (a) purchase NFTs and (b) earn some reward (e.g., NFTs or tokens) by playing the game, the reward portion may be subject to the prize regulation. There is an argument that depending on the game design, the reward may not be considered an extra (premium) and may not be subject to the Premiums Law. |

The following is a discussion of each legal issue.

(a) Where is the problem?

Under blockchain games, the game operator frequently sells game characters, items, weapons, and land etc. as NFTs to users in exchange for ETH or other crypto assets.

Japanese law does not regulate sales of pure NFT, but regulate sales of crypto assets and sales of securities. Thus, whether sold tokens are not deemed as crypto assets or securities are crucial issue.

(b) What are crypto assets?

Under the Fund Settlement Act, the seller, Crypto Asset is defined as follows:

| Definition of Crypto Assets (Article 2 Section 5 of the Fund Settlement Act |

| Definition of Type 1 Crypto Asset |

| A property value that is recorded in electronic record and transferred electrically, that can be used to pay for the purchase of goods or receive services to an unspecified person, and that can be purchased and sold to an unspecified person (excluding some stable coins and securities). |

| Definition of Type II Crypto Assets |

| Crypto Asset that is recorded in electronic record and transferred electrically which can be mutually exchanged with the Type I Crypto Asset with an unspecified party (excluding some stable coins and securities). |

Selling or providing custody of crypto assets are highly regulated and must generally be handled by registered crypto asset exchange operator and also it is not feasible for a blockchain game operator to obtain registration.

At this moment, whether tokens are considered as crypto assets is determined by the number of issued tokens and whether the tokens can be used as some form of payment. NFTs are generally not considered as crypto assets, but if a game operator says it is an NFT, and the NFT has payment features etc., it may be considered a crypto asset.

(c) What are Securities?

Japanese Financial Instrument and Exchange Act (FIEA or Security Act) governs the issuance or sales of securities. Securities includes stocks, bonds, mutual funds, collective investment scheme etc. We have been often asked by blockchain game operators whether it is legal in Japan to sell NFTs, such as land, which generate “income” or “dividend”. If NFTs generate income without the participation of players, they may be classified as securities. Thus, when selling profit-generating tokens, the game should consider including features of players’ effort, such as editing land to attract customers.

(a) General Remarks

The crime of gambling under the Penal Code is established by (1) contesting the gain or loss of property profits by (2) winning or losing by chance. In addition, not only money but also “property interest” is considered to be the object of gambling, and rice, land, and debt collection are all considered to be “property interest” subject to the crime of gambling. Crypto assets are also considered to fall under the category of property interest.

| Article 185 (Gambling) |

| A person who engages in gambling shall be punished with a fine of not more than 500,000 yen or a fine. However, this shall not apply when the betting is limited to betting on objects provided for temporary entertainment. |

(b) Gacha (Loot Box), Reveal and Gambling Law

Some blockchain games have features of Gacha (loot box) and reveal. Users pay money or crypto assets to a gaming company and get NFTs randomly. For example, users pay 1ETH to get a game character NFT. Game characters may include Julius Caesar, Guanyu, Genghis Khan, Napoleon, George Washington etc, and those characters have different strength, powers, rarity etc, and what users can get is not revealed to users.

It was believed that these sales might be considered as gambling because (i) users pay property value, (ii) users receive property value which differs by chance, and (iii) there is winning or losing (of property value) by chance. However, in 2022, blockchain industries talked with a famous criminal law professor and some regulatory authorities and issued the guideline which states certain Gacha and reveal is not considered as gambling. Although the guidelines have no effect to police or criminal courts, the industry is now considering how following the guidelines may reduce the likelihood of criminal penalties.

The requirement is that the issuer and operator of games do not sell the same NFTs at different prices (for example, if the issuer sells NFTs that include Napoleon with 1ETH via Gacha, the issuer is not allowed to sell Napoleon NFT at a different price in another method), and do not buy back NFTs in a secondary market (for example, the issuer cannot buy back Napoleon NFT in 0.5ETH or 1.5ETH). In such cases, there is either winning or losing), and the issuer and operator shall not overstate the value of some NFTs in Gacha over other NFTs in Gacha.

(c) Synthesis

The same theory that applies to Gacha may apply to synthesis, but because synthesis is not discussed in the guidelines, we take a more cautious approach to synthesis.

(a)Initial Start

Developers often ask us of blockchain games if it is possible to give NFTs, game currency, crypto assets, other property to users free as a login bonuses, playing bonus and ranking bonuses etc. When conducting such distribution, it is necessary to consider the relationship with the Premiums and Representation Law.

(b) About the Premiums and Representation Law

The Premiums and Representation Law prohibits the offering of excessive premiums.

Premiums are (1) offered as a means of inducing customers, (2) offered incidental to a transaction, and (3) economic benefits such as goods or money. As the definition of economic benefits is broad, crypto assets, NFTs, in-game currencies, and other benefits might be considered as economic benefits.

Excessiveness will vary depending on whether the sweepstakes is general sweepstakes, joint sweepstakes, or all-inclusive sweepstakes, Still, it will be based on the following criteria to the extent that it is considered relevant to the game.

| Description | Example | Limits on Premium and Prizes | |

| Total Prizes | Offering prizes to anyone who uses the products or services or visits the store, not through sweepstakes. | Gifts for all purchases, gifts for all visitors, etc. | Transaction value less than 1,000 yen – Premiums up to 200 yen. Transaction value is over 1,000 yen – Premiums are capped at 2/10ths of the transaction value |

|

General Sweepstakes |

Offering prizes to users of goods or services by chance, such as lotteries, or by the superiority of specific actions. | In-store raffles, quiz and game competitions. | Transaction value less than 5,000 yen – 20 times the transaction value. Transaction value of more than 5,000 yen – 100,000 yen. (Both are capped at 2% of the total expected sales amount) |

(c) Ranking Rewards and the Premiums and Representation Law

In traditional smart phone games, the top-ranking players frequently receive in-game currency. The economic value of in-game currency has been treated as zero or very low by game operating companies, and there is no issue under the Premiums and Representation Law.

In blockchain games, crypto assets and NFTs, which can be sold outside of the game might be given as prizes. In this case, the general sweepstakes restrictions apply. The transaction value determines the amount of the prize. Although it is difficult to determine how much the transaction value is, a reasonable approach would be to set the minimum charge as the transaction value and allow rewards of up to 20 times the minimum amount or 100,000 yen, whichever is lower.

(d) Play to Earn and the Premiums and Representation Law

If we consider a Play to Earn game as a game where players (a) purchase NFTs or game currency and (b) earn some reward (e.g., NFTs or game currency) by playing, the reward portion may be subject to the Premiums Regulation.

However, whether earned NFTs or game currencies will be considered “premium” is unknown. There is an argument that the Premiums Law does not apply to Play to Earn games because the rewards are not “extras (premiums),” but rather the purpose of purchasing NFTs and playing the game itself. Lottery winnings and game-play prizes, for example, are not considered “premiums,” but rather “the purpose” of the transaction itself (gambling law shall be discussed lottery winnings and game-play prizes). This issue has not been resolved in Japan, and careful deliberation is required.

Reserved Matters

The contents of this document have not been verified by the relevant authorities and are merely a description of arguments considered reasonable under the law. It is only the current thinking of our firm, and our firm’s thinking is subject to change.

This document does not recommend using blockchain games or purchasing NFTs.

This document is intended for blogging purposes only. Please consult your lawyer if you need legal advice on a specific case.

Introduction

Clients often ask us whether it is possible to structure a Decentralized Autonomous Organization (DAO) in Japan. Currently, Japan does not have regulations targeting DAOs, unlike Wyoming State or the Marshall Islands. So, we have written this article summarizing what is typically considered when forming a DAO in Japan.

1.1 What is DAO?

A decentralized autonomous organization (DAO) is a new legal structure with no central authority and members committed to acting in the organization’s best interests. DAOs are used to make decisions in a bottoms-up management style and have gained popularity among cryptocurrency enthusiasts and blockchain technology.

1.2 Classification of DAOs

There are several classifications of DAO described below:

| 1. Investment DAO Investment DAOs are for-profit DAOs aim at co-investing in a project. They are more likely to attract funds than Grant DAOs because they aim to generate profits mainly through “economic capital.” Examples: Genesis DAO, The LAO, BitDAO, etc. 2. Grant DAO The community contributes monies to the grant pool and votes on funds allocation and distribution decisions in a Grant DAO. Innovative DeFi projects are funded using these DAOs, showing how decentralized communities are more flexible with funding than traditional organizations. Examples: MolochDAO, MetaCarteDAO, Aave Protocol, Uniswap Grants, etc. 3. Protocol DAO When tokens serve as a voting metric for implementing any changes in the protocol, such a governance structure represents protocol DAOs. For instance, MakerDAO has revolutionized the DeFi space with its DAI stablecoin. Examples: Maker, Compound, Uniswap, Aave, Yearn, Sushi, etc. 4. Service DAO A Service DAO is a decentralized working group. They can receive tokens as compensation for their projects. Examples: RAID GUILD, DXdao, PartyDAO, etc… 5. Social DAO A Social DAO offers digital democracy where opinions are heard, and people can share common interests. Example: Bored Apes (BAYC) 6. Collector DAO Artists who use nonfungible tokens (NFTs) to create art rely upon collector DAOs to establish ownership of their art. Example: PleasrDAO 7. Media DAO Media DAOs allow product owners of content (i.e., readers) to contribute directly without involving advertisers for the native token as a reward in return for their contributions. Example: Fore Front (FF), Bankless DAO, etc… Source https://cointelegraph.com/daos-for-beginners/types-of-daos |

1.3. Example of an Existing Overseas Law

A few places where DAOs are regulated are Wyoming State and the Marshall Islands. Below is a short description of forming a DAO in the Marshall Islands.

The Legal Form of a DAO on the Marshall IslandsMarshall Islands proposes a non-profit corporation (limited liability company) as a legal entity form for DAO, which stands out from the general practice to establish DAO as a foundation. Such a company is established in compliance with the general corporate law of the Marshall Islands with specific features that:

How does this work?Generally speaking, such a company works as a limited liability company managed by its members. It has three essential constitutional documents: Certificate of Incorporation, Operating Agreement, and Charter of the Company.The Operating Agreement should include the most crucial matters of your DAO management:

You can amend any of these matters by the members’ decision in compliance with the procedure prescribed in the previous version of the Operating Agreement. Registering a Marshall Islands LLC for DAOHere’s what the process of establishing a legal wrapper for DAO on the Marshall Islands looks like:

The above is a reference from Taras Zharan Web 3 Virtual Legal Officer. https://legalnodes.com/article/marshall-islands-llc-as-a-dao-legal-wrapper |

2.1. Points to Consider

When structuring a DAO, one must consider the financial regulations and the legal form characteristics.

Here are several points to keep in mind:

1. Security regulation under the Financial Instrument and Exchange Act (“FIEA”) may apply when tokens have the possibility of dividends or redemption of the principal of more than 100% (dividends and redemption of the principal of more than 100% are from now on collectively referred to as “dividends, etc.”). As a general rule, token sales of such DAO must be conducted by a Type 1 Financial Instrument and Exchange Business Operator (“Type I license”) or by obtaining a Type 2 Financial Instrument Exchange Business Operator license (“Type II license”).

2. When selling Fungible Tokens without dividends, etc., it is necessary to have a Crypto Asset Exchange Operator conduct the sale or to obtain a Crypto Asset Exchange Operator license.

In contrast, these financial regulations generally do not apply when selling NFTs without dividends, etc.

3. You also need to consider the tax benefits. If you want to pursue tax advantages in an Investment DAO with dividends, etc., you can use a partnership or GK-TK scheme. If tax advantages are not particularly important, an association without rights, a general incorporated association, or a limited liability company can be considered a scheme to issue tokens. For the issuance of Fungible tokens or NFTs without dividends, etc., it may be better to have no particular legal structure.

2.2. Reference Table of Conclusions

The table below summarizes the legal scheme and financial regulations that should be considered in establishing a DAO.

The following regulations apply to token sales of Investment DAOs with dividends, etc. (assuming dividends or principal redemption of more than 100%).

| Type of Member’s Rights | Form under Japanese Law | Free distribution of Tokens | Token Sale | Investment Management |

| DAO member’s rights as shareholders’ rights in Limited Liability Companies and Joint-stock Companies | Tokenization of shareholders’ rights of limited liability companies, etc. | Free distribution of the shareholders’ rights is not allowed under corporate law, etc. |

Sales by a third party for an issuer need a Type I license. A Type II license is necessary for the self-offering of a limited liability company. No license is required in the case of self-offering of a joint-stock company. In the case of solicitation of 50 or more people, there needs to be a submission of a registration statement regarding securities, etc. |

No regulation |

| DAO member’s rights (with dividends), not including shareholders’ rights | TK investment, partnership investment, tokenization of rights that are difficult to classify into prescribed legal forms, etc. | Unregulated |

Sales by a third party for an issuer need a Type I license. Self-offering needs a Type II license. In the case of solicitation of 50 or more people, there needs to be a submission of a registration statement regarding securities, etc. |

No regulation (Possibility of Investment Management Business license in the case of securities investment) |

On the other hand, a DAO without dividends, etc., is also possible. Its regulations are as follows:

| Tokens/NFT | Free Token Distribution | Sale of Tokens | Investment Management(Assuming no dividend) |

| Utility Tokens | No regulation | Crypto Asset Exchange Business regulation | No regulation |

| NFT | No regulation | No regulation | No regulation |

With respect to possible legal forms for DAOs, the following comparisons can be made:

| Status | Legal Form | Limited Liability | Is it possible to distribute? | Avoid Double Taxation | Others, Comprehensive Evaluation |

| No Legal Entity Status | Association without rights +Tokens with unclear rights | 〇? | 〇 | × |

△~〇 High degree of freedom. A good scheme if there is no problem with double taxation. |

| Civil Law Partnership + Partnership Equity Token | × | 〇 | 〇 |

△~〇 High degree of freedom. A good scheme if there is no problem with limited liability. |

|

| Investment Business Limited Liability Partnership + partnership Equity Token | 〇 | 〇 | 〇 |

× Although other points are reasonable, there are restrictions on investment destinations and businesses, such as not being able to purchase NFTs. It’s usually hard to use this scheme as DAO. |

|

| Limited Liability Partnership + Partnership Equity Token | 〇 | 〇 | 〇 |

× There are valid points; however, to use as a DAO is problematic because of the need to register the name of the union member. |

|

| DAO has Legal Entity Status |

Corporation (*1) + Tokenization of Anonymous Partnership (e.g., TK-GK scheme) |

〇 | 〇 | 〇 | △ It is necessary to operate in accordance with the Companies Act and the General Incorporated Associations Act. It should be noted that TK holders do not have the right to instruction. The good point is that there is no double taxation and limited liability. |

|

Corporation (*1) + Token with unknown rights |

〇? | 〇 | × | △ ~ 〇 It is necessary to operate under the Companies Act and the General Incorporated Associations Act. Besides that, it has a high degree of freedom and is a good scheme if you don’t mind the double taxation problem. | |

|

Corporations (*1) + Tokenization of shareholders rights (*2) |

〇 | 〇(× For general incorporated associations) | × |

× Is there a low degree of freedom due to the need to operate per the Companies Act and the General Incorporated Associations Act? For example, it is necessary to manage members as shareholders. |

*1 Legal entities include limited liability companies, stock companies, and general incorporated associations. LLCs are generally easier to establish and operate than joint-stock companies. If you want to have a more public image, use a general incorporated association.

*2 Membership rights of a limited liability company, stocks of a stock company, membership rights of a general incorporated association.

2.3 Tokenization of Rights

Tokenization of rights of funds or partnership, where there is an investment of funds (including money and crypto assets), investment management, dividends, or redemption of the principal of more than 100%, would be broadly considered a collective investment scheme (fund) under Japanese law. Below is the summary of the Definition of a Collective Investment Scheme.

| Summary of Definition of Collective Investment Scheme |

| Rights that satisfy the following (i) to (iv) |

| (i) Rights under a partnership agreement as defined in Article 667(1) of the Civil Code, a silent partnership agreement as defined in Article 535 of the Commercial Code, an investment limited partnership agreement as defined in Article 3(1) of the Act on Limited Liability Partnership Agreement for Investment Business, or a limited liability partnership agreement as defined in Article 3(1) of the Act on Limited Liability Partnership Agreement for Investment |

| (ii) The existence of a business (the “Invested Business”) in which money (including cryptographic assets) contributed or contributed by the person who has such rights (the “Investor”) is allocated to the Invested Business; |

| (iii) The investors are entitled to receive dividends of profit generated from the invested business or distribution of assets related to the invested business; |

| (iv) There are no exceptional circumstances, such as all investors being constantly involved in the business. |

The revised Financial Instruments and Exchange Act, which came into effect on May 1, 2020, created the legal concept of Electronic Record Transfer Rights. The rights of tokenized collective investment schemes usually fall under the Electronic Record Transfer Rights below.

| Outline of Definition of Electronically Recorded Transfer Rights |

| Rights that satisfy the following (i) to (iii) but exclude (iv) (Article 2, Paragraph 3 of the FIEA): |

| (i) Rights listed in each item of Article 2, Paragraph 2 of the FIEA (funds, trust beneficiary rights, members’ rights of general partnerships, limited partnerships, limited liability partnerships, etc.); |

| (ii) When they are expressed in property values that can be transferred through an electronic data processing system; |

| (iii) When recorded in electronic devices or other objects by electronic means; |

| (iv) Cases provided in the Cabinet Office Ordinance have considered the nature of distribution and other circumstances. |

The sale of this electronic record transfer right requires a Type 1 Financial Business registration. If soliciting more than 50 people, it will be a public offering (Article 2, Paragraph 3 of the Financial Instruments and Exchange Act), and a securities registration statement must be submitted based on Article 5 of the FIEA.

If the sale is limited to qualified institutional investors or wealthy people of 49 or less, and even if there is resale, there are technical restrictions so that other people cannot become DAO token holders.

When the Investment DAO is formed, it can be sold in such a limited form at first, and after it grows, it can be sold to the general public while complying with increased regulations.

2.4 Tokenization of Company Membership Rights and Financial Registration Regulations

Regarding tokenization of company membership rights, a Type I FIBO license is necessary when a third party sells the rights, and Type II is essential in the case of self-solicitation. In the case of tokenization of company membership rights (shareholders rights) of a joint stock company, a Type I license is necessary in the case of solicitation by a third party, and no license is required in the case of self-solicitation.

2.5 Regulations on Public Offerings, etc.

If any of the following applies, it becomes a public offering. In principle, it is necessary to submit a securities registration statement.

| (i) When soliciting the acquisition of securities from 50 or more persons (excluding Qualified Institutional Investors (QII) in the case there are restrictions on resale other than QII); (ii) When it does not fall under any of the following categories: Private Placement for QII, Private Placement for Professional Investors, and Private Placement for Small Groups. |

2.6 Financial Regulations for DAOs without Dividends

If DAOs have no dividends, etc., they are not considered securities, but different financial regulations may apply.

| Tokens/NFTs | Free token distribution | Token Sales | Investment Management (Assumption without dividends) |

| Utility Tokens | Unregulated | Crypto Asset Exchange Business License | Unregulated |

| NFTs | Unregulated | Unregulated | Unregulated |

Disclaimer

The content of this article has not been confirmed by the relevant authorities or organizations mentioned in the article but merely reflects a reasonable interpretation of their statements. The interpretation of the laws and regulations reflects our current understanding and may therefore change in the future. This article does not recommend investment in DAO. This article provides merely a summary for discussion purposes. If you need legal advice on a specific topic, please feel free to contact us.