Category Archives: digital assets

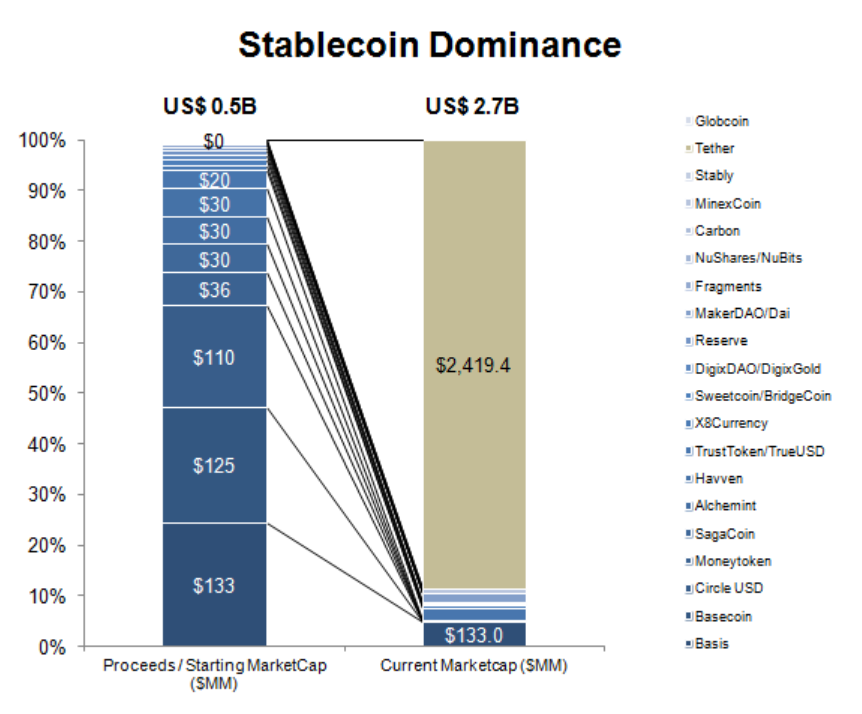

According to proponents of stable coins, the volatility of bitcoin and other cryptocurrencies is one of the biggest barriers to mainstream adoption. Stable coins come with the promise to remove these barriers and are therefore praised as the Holy Grail of Crypto. As of the time of writing, stable coins have reached a market capitalization of USD 4 billion. With the rise of decentralized exchanges without links to the traditional financial system, this amount is likely to increase. Despite the overall success of stable coins globally, none of the big projects has been listed on cryptocurrency exchanges in Japan yet.

In the following, we will explain the different types of stable coins and assess the regulatory environment for each model in more detail.

Types of Stable Coins

“Stable coin” is an umbrella term describing crypto assets which are stable relative to a predetermined asset – most commonly the US Dollar. In general, there are three types of stable coins: IOU[1] models, on-chain collateralized models, and seigniorage models.

The examples used in this article are for illustrative purposes only.

1.1 IOU models

IOU models currently dominate the stable coin landscape. This is likely to be attributed to the simplicity and clarity of the model. While a look under the hood shows significant differences in design, all IOU models have in common that there is a central entity that issues tokens which represent a redeemable certificate against the issuer for the benefit of the token holder. To ensure the stability of the token, each token is generally fully backed by a fiat currency or another real-world asset. In few cases, a mere guarantee is made by the issuer to buy back tokens at a predetermined price.

In the case of TrueUSD, tokens are freshly minted when users wire funds to a third-party escrow account and burned when US Dollars are redeemed. This mechanism ensures parity between TrueUSD in circulation and the US Dollars held in escrow accounts. A similar mechanism is deployed by Libra[2], where each token is backed by reserves. New tokens are only minted if authorized resellers inject money into the reserves. Conversely, tokens are destroyed when demand contracts. Since the tokens are backed by a basket of fiat currencies rather than a single fiat currency, there will be fluctuations in price as a result of FX market movements.

Tether – by far the most successful but also one of the most controversial stable coin projects[3] – mints new tokens irrespective of user payments. Yet, similar to TrueUSD, the project promises to maintain a one-to-one ratio between its stable coin USDTether and US Dollars held as reserves.

In Japan, a project known as JPYZ was launched in 2017. Unlike the projects mentioned above, JPYZ are not backed by Japanese yen. Parity with JPY is maintained by a guarantee of the issuing entity to make a purchase order of each token for a price of JPY 1 on listed exchanges. The project is described as a social experiment and has not scaled as much as some of the USD stable coins yet.

Token(s): stable coin

1.2 On-chain collateralized models

On-chain collateralized models require a complex system of smart contracts, different kinds of tokens, oracles, and external actors to ensure their coin remains stable. MakerDAO, for example, requests its users to transfer crypto assets to a smart contract. The smart contract then issues a loan in the form of stable coins (DAI) and effectively locks the collateral in the smart contract until the loan is paid off.

The target price for DAI is set to USD 1 and used to determine the value of collaterals locked in the smart contract. Given the volatility of the collateral MakerDAO requires all loans to be over-collateralized. Where the collateral-to-debt ratio falls below a certain threshold, the position is automatically liquidated, and the collaterals sold on the market. This ensures that DAI always remains stable relative to the US Dollar.

A second type of token – Maker Token (MKR) – is used for the payment of a stability fee. This fee must be paid in addition to the debt in order to release the collateral from the smart contract. MKR tokens further play a central role in the governance of the Maker Platform, by giving each token holder voting rights (e.g. for the appointment of oracles and the determination of the stability fee).

Main tokens: stable coin, hybrid governance / utility token

1.3 Seigniorage models

Seigniorage models are based on the quantity theory of money. To keep the token price stable compared to a reference currency or another reference value, the token supply is adjusted continuously depending on demand and supply. In phases of inflation, the token supply is contracted automatically to bring prices back to the original level. Conversely, the token supply is expanded in phases of deflation.

In the case of Basis[4] the stable coins (Basis) were pegged to the US Dollar. To maintain the peg, the Basis supply was controlled by additional tokens – share tokens and bond tokens. The bond tokens were auctioned off for prices less than one Basis when the supply had to contract. When the system determined that an expansion of the Basis supply became necessary, holders of bond tokens received one Basis for each bond token in a first-in-first-out order. In cases where the bond tokens were not sufficient to expand the token supply, holders of share tokens participated in the issuance of new Basis according to their overall share tokens in the system.

Main tokens: stable coin, bond tokens, share tokens

2. Legal Classification and Consequences

In the following, we will analyze each model in more detail. Where a model involves more than one token, the additional tokens are considered in our analysis as well.

2.1 IOU models

In an IOU model, a single token – the stable coin – is issued. Depending on the design of the token and the underlying business model, a token might either be classified as a prepaid payment instrument, money order, or virtual currency.

2.1.1 Prepaid Payment Instrument

The Payment Services Act (‘PSA’) defines prepaid payment instruments inter alia as signs which are recorded electronically in exchange for consideration. Depending on whether the signs can be used for the purchase of goods and services from the issuer or the issuer and persons designated by the issuer, a prepaid payment instrument may either be classified as a prepaid payment instrument for own business or a prepaid payment instrument for third-party business.

In most cases, stable coins do not constitute prepaid payment instruments since they are not issued for the purchase of goods and services within a predefined ecosystem. Instead, they can be accepted for payment – irrespective of contractual relationships with the issuer – by anyone. The mere fact that stable coins can only be redeemed by users who have passed the know-your-customer procedure of the issuer does not lead to different results.

Also, the fact that stable coins issued under the IOU model can generally be redeemed for fiat currency speaks against the classification as a prepaid payment instrument. According to the PSA “issuers of prepaid payment instruments must not make any refunds” except in cases specified in the PSA. Typical cases are the redemption of small amounts and cases where the user cannot continue to use the prepaid payment instrument for inevitable reasons (e.g. discontinuation of the business of the issuer).

2.1.2 Money Order

Stable coins issued in exchange for fiat currencies that can be redeemed by the token holder are likely to be classified as a money order. While there is no legal definition in the PSA or the Banking Act, a money order is commonly understood as a payment order for a certain amount of money. The amount indicated on the money order must generally be paid upfront and can only be cashed by the person shown as the recipient in the money order. Tokens issued under the IOU model do however, not include a recipient. Instead, they may be redeemed by anyone who owns the private key corresponding to the respective token. As such stable coins are comparable to blank money orders with enhanced safety features and increased negotiability. Even slight changes to the underlying business model may lead to different results (see item 2.1.3 below).

Tokens that are classified as money orders are not regulated themselves. For entities involved in the sale, transfer or redemption of the token, the law may require, however, that these entities hold a banking license or are registered as a transfer service provider under the PSA.

2.1.3 Virtual Currency

In some cases, stable coins issued under the IOU model may also constitute virtual currencies. The PSA distinguishes between Type I and Type II virtual currencies. Type I virtual currencies are defined broadly as property value that

- can be used for payment to unspecified persons,

- can be purchased from and sold to unspecified persons, and

- can be transferred electronically.

Type II virtual currencies are defined as values that can be mutually exchanged for Type I virtual currencies with unspecified persons and which can be transferred electronically.

Currencies and currency denominated assets are explicitly excluded from Type I and Type II virtual currencies.

Since stable coins issued under an IOU model are likely to be classified as currency denominated assets, they cannot be classified as Type I or Type II virtual currencies.

Even slight changes to the underlying business model may, however, lead to a completely different result. This can be seen from JPYZ. Different from the other IOU models, JPYZ tokens are not refunded by the issuing entity but bought back for a guaranteed price through an exchange – JPY 1 for JPYZ 1. This has led the Financial Services Agency (FSA) to classify JPYZ as virtual currencies within the meaning of the PSA.

Entities issuing stable coins that constitute virtual currencies must register as a virtual currency exchange business in Japan.

2.2 On-chain collateralized models

On-chain collateralized models typically involve more than one token. In the case of MakerDAO, this includes a stable coin and a hybrid utility governance token.

Stable coins issued under an on-chain collateralized model are likely to be categorized at least as Type II virtual currencies. This is due to the fact that they can be mutually exchanged with Type I virtual currencies with unspecified persons. The mere fact that there is a soft peg to the US Dollar or other fiat currencies does not make the stable coin a currency denominated asset. The peg serves as a stability mechanism only and does not contain the promise to make a refund in US Dollar or another fiat currency.

Governance tokens which can typically be mutually exchanged with Type I virtual currencies are generally considered Type II virtual currencies.

2.3 Seigniorage models

Stable coins issued under seigniorage models are likely to be classified as virtual currency Type II. Insofar, reference is made to the explanations under item 2.2. above.

Bond and share tokens necessary for the adjustments to the money supply may be classified as securities under the Financial Instruments and Exchange Act (‘FIEA’). The marketing of such securities generally requires registration as Financial Instruments Business Service under the FIEA.

Where bond and share tokens can be mutually exchanged with Type I virtual currencies, they are further deemed Type II virtual currencies.

A listing on one of the registered cryptocurrency exchanges is not possible for securities under the current regulations.

3. Conclusion

This article only gives a high-level overview of the current regulatory environment for different stable coin models in Japan. Even slight changes to the token design or underlying business model may lead to completely different results. Issuers of stable coins are therefore well advised to consider their model carefully – and in cases where the stable coin is on the market already to assess whether the stable coin can be marketed and eventually listed in Japan.

If you want to learn more or should you need legal or regulatory advice, please feel free to contact us directly under s.saito@innovationlaw.jp.

DISCLAIMER

The stable coins mentioned in this article are used for illustrative purposes only. Given the format of the article not all details of the token design and underlying business model have been considered, so that the results of the assessment may deviate from the results by the regulator or a legal opinion prepared for the respective project. By no means, the explanations should be understood as a legal opinion regarding the stable coins mentioned in this article.

FOOTNOTES

[1] IOU stands for I owe you.

[2] Libra has not gone online yet and only published its whitepaper recently.

[3] According to the terms and conditions of Tether, “the composition of the reserves used to back tether tokens is within the sole control and absolute discretion of Tether” and “may include other assets and receivables from loans made by Tether to third parties, which may include affiliated entities”. Tether has not provided audited accounts yet and has repeatedly been accused of market manipulation in the past.

[4] On December 13, 2018, Basis announced that US regulations had a serious negative impact on their ability to launch Basis and forced them to shut down before the project was launched. All funds were returned to their investors.

Japan’s Financial Services Agency (the “FSA”) imminently contemplates reforming the crypto regulations to address the problems that arose after Phase 1 of the virtual currency legislation, effected in April 2017. The FSA published a draft bill for the amendment of the virtual currency regulation on March 15, 2019. Stated below is our current understanding of the amendment. Please note that as the national diets will discuss the draft from now and the FSA will draft subordinated provisions of the laws from now, there is still some uncertainty on the amendment, and our analysis is expressly subject to changes in the future.

I Background Information about Japanese Crypto Regulation

1 Existing crypto legislation and regulations

The Payment Services Act (the “PSA”) and the Act on Prevention of Transfer of Criminal Proceeds (the “AML Act”), as amended together in April 2017, are the base of the Phase 1 virtual currency legislation, as supplemented by the related ordinances, orders, and guidelines (most notably the Guidelines for Administrative processes concerning virtual currency exchange service providers (FSA Guidelines)).

2 The Payment Service Act

The PSA (so amended in 2017) is an act which currently regulates a virtual currency exchange. The PSA stipulates “Virtual Currency,” “Virtual Currency Exchange Service,” and “Virtual Currency Exchange Service Provider” therein. It requires registration of Virtual Currency Exchange Service Providers, and the FSA regulates and supervises them.

The PSA will be amended and involve more detailed regulation on crypto exchanges and new regulation on crypto custody business.

3 The Financial Instruments Exchange Acts (the “FIEA”)

The FIEA regulates financial instruments, which typically include

securities/derivatives, financial instruments, exchange business and operators thereof.

Currently, virtual currency does not fall under securities, in principle. Some STO tokens fall under collective investment schemes (funds) that are securities (see item 7 below).

Margin trading of virtual currencies (NDF, leveraged trades, physically settledtrades by loans in virtual currency) are currently non-regulated through FIEA.

4 The AML Act

The Act on Prevention of Transfer of Criminal Proceeds (so amended in 2017) has subjected VC exchanges to the AML/CTF regulations and imposed such duties as customer identity verification at the time of the transaction, etc.

5 Self-Regulatory Organization

In April 2018, sixteen (16) registered VC exchanges joined to establish a selfregulatory organization, the Japan Virtual Currency Exchange Association (the “JVCEA”). In October 2018, the JVCEA got certified by FSA as a Certified Association for Payment Service Providers under PSA.

JVCEA established the self-regulation rules in furtherance of the existing regulations that are based on, amongst others, PSA, AML Law and FSA Guidelines with a view to better protect users. Examples of self-regulation are as follows.

- Handling of virtual currency

- User property management

- Management of system-risk and information security

- Contingency

- AML/CFT

- Complaint processing and dispute processing

- Solicitation and advertisement

- User management

- Order management system

- Prevention of illicit transactions

- Management system of virtual currency-related information

- Financial management

6 The status and prospect of pending Registration of Exchanges

Currently, to earn a VC exchange license is perceived to be staggeringly

burdensome for leanly staffed startups. The screening standard now imposes a heightened level of internal control and security, so that no applicant may escape hiring compliance officers, AML officers and internal auditors who are versed with the industry and drafting of internal rules that are extensive and voluminous.

It is said that 190 companies have approached the FSA to take an exchange license, but no new exchanges were eventually approved through 2018. In January 2019, Coincheck Inc. finally got registered, and it is rumored several others will get the license in 2019.

7 Current ICO /STO (Security Token Offering) regulation

Currently, the ICO is subject to the regulation of the PSA. For certain STOs, the regulation of the PSA and the regulations of the FIEA are superimposed.

In December 2017, the FSA interpreted that ICO tokens may broadly be listed as corresponding to “virtual currency. ” As a result, registering a “virtual currency exchange business” and “notification of coin” has become required for the sale of ICOs in Japan. It is difficult to comply with these regulations, and no lawful ICOs have come out in Japan since December 2017.

An STO is deemed to be a kind of ICO, and the same regulation applies. In addition to the PSA regulation, FIEA regulations are applied to tokens that are paid in cash and pay dividends or principal redemption of 100% or more as collective investment schemes.

II Proposed Amendments to the Law

1 General Information

1.1 Which laws will be amended?

The PSA and FIEA will be amended.

1.2 Why crypto regulations are being reformed

Japan had massive cryptocurrency hacking incidents against two major Japanese crypto exchanges in 2018—Coincheck in January and Zaif in September.

After the Coincheck hack, the FSA tightened its oversight of crypto exchanges, including imposing stricter registration requirements and on-site inspections. It handed out many business improvement orders and suspended a few exchanges.

In light of highly volatile cryptocurrency prices and explosive trading volumes in 2017, a surge of ICOs in 2017, and hacking incidents in 2018, FSA created a Study Group on Virtual Currency Exchange Services in March 2018 to discuss appropriate crypto regulations. After eleven (11) sessions of discussion, the group published a final report last December. The FSA drafted bills based on this report and the national government submitted the draft to the national diets in March 15, 2019.

1.3 When will the amendments be enacted?

The timeline still remains uncertain. Quite a few people seem empirically to infer the schedule as follows.

- The national government submitted the amended bill to the national diets in March 15, 2019, and the national diets will discuss them.

- The national diets will approve the bill around this May.

- The FSA will draft government ordinances and guidelines which are subordinated rules of the amended law around the end of 2019. They will be on public comment procedure and be finalized around March 2020.

- The amended law will be valid within one year after the enactment of the acts (i.e.around April or May 2020).

- Some of the new regulations, such as regulation on custody and derivative, might have a six (6)-month transition period after the enactment.

1.4 Way of Calling of Virtual Currency will be changed to Crypto Asset

The way of calling of Virtual Currency will be altered to Crypto Asset with the PSA amendment. In this memorandum, we will call virtual currency crypto assets hereafter.

2 Exchange Business

2.1 Additional Duty Imposed on Exchanges

Exchanges will have the following requirements in addition to the current requirements:

- to establish and publish policy on incidents of virtual currency thefts

- to hold virtual currencies that are not less than the value of the customer’s virtual currencies in hot wallets (if any) as the exchange’s own assets

- to trust customers fiat into a trust company

- to disclose financial statements publicly

- to publish, when conducted, OTC deals with customers as well as bid prices, ask prices, and bid-ask spreads for such OTC deals, etc.

- to refrain from making excessive advertisements, misrepresentations, conclusive assessments, cold calls, inadequate solicitations in light of the customer’s knowledge, etc. or advertisements and solicitations to induce speculative trading

- to replace the current ex-post notification requirement of any change in tradable virtual currencies with a prior notification requirement thereof in order to exclude problematic virtual currencies

We believe that one of the most onerous burdens is the second one. The definitions of “hot wallet” and “cold wallet” are not stipulated in the law, and we believe that SRO will discuss it.

If an exchange holds 5% of users’ BTC in a hot wallet, such exchange needs to have the same amount of BTC as its own asset. As there is little hedge market, an exchange should owe a volatility risk of crypto. An exchange shall consider how much it holds in a hot wallet and how to manage the volatility risk of its own crypto in order to do a healthy business.

2.2 Preferential Right of Customer

The amended PSA stipulates a new right of customers. Customers will have the right to receive a preferential return of crypt assets they deposited with an exchange and the exchange segregated upon its insolvency.

2.3 Regulation on Unfair Trading

The amended FIEA will regulate unfair trading. The regulation applies not only exchanges but every person, including customers.

Prohibition of unfair trading includes following but does not include prohibition of insider trading:

- prohibition of unfair trading

- prohibition of fraudulent acts, spreading rumors, using fraudulent means or intimidation

- prohibition of market manipulation

3 Custody Business

3.1 Currently, custody business is not regulated.

The current PSA regulates virtual currency exchange businesses and does not include businesses that just provide a custody service. The definition of a virtual currency exchange business is as follows, and does not include mere custody business.

- Sale and purchase of VC (i.e., an exchange between VC and fiat currency) or exchange of a VC into another VC;

- An intermediary, brokerage, or agency service for the acts described above (i); and

- Management (custody) of a fiat currency or VC on behalf of the users/recipients in relation to the acts described above in (i) and (ii).

3.2 Custody businesses will be regulated

The amended PSA will regulate custody businesses. The definition of custody is “to manage crypto assets for others except for the case such business is allowed in other laws). ” Custody businesses will not be able to do business to Japanese residents without a license.

3.3 What kind of custody businesses will be regulated?

As the definition of “custody business” is unclear, the types of custody businesses that will be regulated are still uncertain.

Generally speaking, we believe that businesses that hold customers’ secret keys and sends crypto for customers will be regulated. However, whether or not multi-sig custody is regulated, a company that sets a node for the Lightning network and holds its customers’ crypto is uncertain.

3.4 Will a software wallet service that does not hold customers’ secret keys be regulated?

We believe no.

3.5 Regulations a custody business operator should obey.

It is believed that the custody business operator should abide by similar obligations to virtual currency exchange, such as those below.

- the requirements of registration

- the establishment of an appropriate internal control system・the requirements of segregation of customers’ virtual currencies

- external audit of customer audit, customer asset segregation, and financial statements

- to establish and publish its policy on incidents of virtual currency thefts

- to hold virtual currencies which are not less than the value of the customer’s virtual currencies in hot wallets (if any) as its own assets

- to give customers the right to receive a preferential return of the virtual currencies they deposited with custody upon its insolvency [that takes precedence over the right of general creditors]

- not to handle virtual currencies recognized to be likely to hinder user protection and/or appropriate and reliable performance of the virtual currency exchange business

- the know-your-customer (KYC) requirements under the AML law

- suspicious activity reporting requirements under the AML law

4 Crypto Derivative

4.1 What is the current regulation on crypto derivatives?

As has been said in I. 3. above, there is no regulation by law on crypto

derivatives right now. The JVCEA, however, exerts control over crypto derivatives through the provisions in its self-regulation rules.

4.2 Does FIEA regulate crypto derivative transactions? Will the FIEA regulate crypto derivative transactions?

The FIEA regulates derivatives such as foreign exchange derivative

transactions (IR/FX-related derivatives), equity derivatives (securities-related derivative transactions), and credit derivative transactions. The regulations on derivatives only apply a stipulated derivative on FIEA, and the crypto derivative is not stipulated in FIEA. We believe the amended FIEA will add a crypto derivative in the enumeration.

4.3 What kind of regulation will a crypto derivative dealer be required to obey?

Currently, a forex derivative dealer should register as a Type I Financial Instruments Business Operator. This means registration as a full-fledged security company, and it is difficult to take the license.

4.4 What will be a maximum leverage ratio?

It is currently discussed that a maximum leverage ratio should be two (2) times.

4.5 Will there be any exemptions to a license?

Derivative dealers are currently exempted from taking a license if they only trade with institutional investors such as banks, security companies, and corporations that have more than JPY1 billion capital. We expect that a similar exemption applies to a crypto derivative dealer.

5 Regulation of ICO and STO

5.1 The regulation of ICOs

As for the regulation of ICOs, no major changes are being made by the

legislative reform at this time. To conduct/carry out ICOs, it is believed that the registration of crypto assets exchanges plus the filing of the coins with the FSA will be required. The registration requirement can be met by either the ICO issuer himself or by an ICO sales broker. The ICO coins that will be approved for sale in Japan are being discussed by the FSA and JVCEA, and it is believed that the JVCEA will publish the rules governing the self-regulation of ICOs in the near future.

5.2 The regulation of STOs

FIEA now defines STOs independently of ICOs under this amendment. Since an STO is clearly positioned as a Security, FIEA applies. A seller of an STO other than the issuer (such as an STO broker) must register as a Type I Financial Instrument Operator. If an issuer sells STOs directly, the issuer must register as a Type II Financial Instrument Operator, which is less complicated. FIEA regulations such as the duty to disclose information, the regulation of sales, and invitation will apply.

Currently, unlike ICOs, there are exemption provisions for the sale of securities, such as Regulation D and Regulation S in the U. S. The sale of securities only to qualified institutional investors or selling securities to a small number of people are exempt from some regulations. It seems that such exceptions will be applied to the sale of STOs, but the details of these exceptions will only be defined in future ordinances.

6 Other

6.1 ETF: I read an article that states that the Japanese government will allow crypto ETF. Is it true?

We do not have any information that the Japanese government will allow crypto ETF. The study group did not discuss crypto ETF, so we do not have any information.

1 Virtual Currency Legislation

1.1 History and statutory framework:

As Japan’s regulatory response to the MtGox failure and the Financial Action Task Force (FATF) guidance in 2015 recommending all virtual currency (“VC“) exchangers be registered or licensed and under the same scrutiny as financial institutions, amendments to the “Act on Settlement of Funds” and the “Act on Prevention of Transfer of Criminal Proceeds” (together with the ancillary amendments to the relevant orders for enforcement, cabinet office ordinances, etc., the “VC Act” or the “Act” hereunder) came into effect as of 1 April 2017 (the “Effective Date“).

1.2 Definition of Virtual Currency

Under the VC Act, the definitions of VC are in two-fold.

| Under the VC Act the term “Virtual Currency” means; (i) financial value (recorded by way of electronic means in the electronic devices etc., excluding any fiat currency or currencies (of Japan or otherwise) and assets denominated in any such fiat currency) that may be used to pay for the goods purchased or rent or the services received to/ as against unspecified person or persons therefor and which may in itself be purchased from and/or sold to the unspecified person or persons (the “Type I VC“). (ii) financial value (recorded by way of electronic means in the electronic devices etc. excluding any fiat currency or currencies (of Japan or otherwise) and assets denominated in any such fiat currency) that may be exchanged as against unspecified person or persons with any such financial value as set out in paragraph (i) above and that may be transported using an electronic data processing system (the “Type II VC“). |

The Type I VC includes Bitcoin, Litecoin, Ether, and other VCs that can be used as a payment method.

The Type II VC may include the vast majority of altcoins, which cannot be used as a payment method at this moment but can be exchanged with Type I VC. A token that can only be exchanged with Type II VC will not fall under the definition of the Type II VC.

The definitions and their interpretation since December 2017 are the topmost focal points among the ICO token practitioners. Both definitions exclude an instrument that pegs to a fiat currency. Thus, even if they use blockchain technology, coins such as the MUFG coin in Japan or Tether will not be regarded as VC.

1.3 Definition of Virtual Currency Exchange Business

The definitions of the VC Exchange Business are as follows:

| Under the VC Act, the virtual currency exchange business (the “VC Exchange Business“) means any of the following acts carried out on a regular basis: (i) Sale and purchase of VC (i.e., exchange between VC and a fiat currency) or exchange of a VC into another VC; (ii) An intermediary, brokerage, or agency service for the acts described above (i); and (iii) Management (custody) of a fiat currency or VC on behalf of the users/recipients in relation to the acts described above in (i) and (ii) |

Below are some examples of business, which might be deemed as conducting VC Exchange Business:

- Exchange in which users can sell and/or purchase VC from other users

- Shop that sells and/or purchases VC

- Operator of Bitcoin ATM

- Operator of ICO (initial coin offering)

- Brokerage firm that intermediates sales or purchase of VC

Below are some examples of businesses that do not fall under VC Exchange Business:

- Person who trades VC for his or her own investment purposes

- Mining firm

- Software developer

- Wallet service provider who does not engage in VC sales/purchases

1.4 VC Act in a nutshell – Regulatory Scope

The Act requires operators of VC Exchange Business (the “VC Exchange Business Operators“) to get registered with the Japanese Financial Services Agency (the “JFSA“).VC Exchange Business Operators are under such duty, pursuant to the Act, as (i) customer identity verification, (ii) accountability to the customers, (iii) segregation of customers’ assets from the proprietary assets, (iv) bookkeeping, (v) compliance, (vi) internal audit, etc.

No person shall, without getting so registered with the JFSA, engage in the VC Exchange Business. Foreign exchange without the registration is also prohibited from conducting VC exchange business to Japanese residents.

1.5 Regulator’s attitude to VC Exchange

Japanese government has long wanted to promote Fintech and new businesses. The Act and the surrounding regulations have been set up after JFSA’s series of discussions over the year with VC exchanges that were themselves starting up. Recently there seems to be a hardening of the attitudes of JFSA in operation of the VC Acts which is somewhat in line with, or presumably reflecting, the surge in price and the change in the global regulatory climate re ICO.

1.6 No arbitrary power

Rest assured the law is clear what it takes to get registered as VC exchange business operators and JFSA has no arbitrary power groundlessly to refuse an application. The regulatory environment in Japan is seen to be, and in fact is, a robust one and more entrepreneurs are swarming. Currently, there are sixteen licensees, and ninety more prospective applicants are said to have approached JFSA to apply next

in a queue.

2 Registration Overview

2.1 Transition period

The Act availed certain interim measures for those VC Exchanges that started their business no later than 31 March 2017 (before the Effective Date). Since such grace period (of 6 months or otherwise) expired, unless the business operator applied for, and such application was officially received by JFSA on or before 30 September 2017, doing VC Exchange Business without being registered is patently illegal. Other early entrants must have filed with JFSA the Notification for discontinuance of Services/ Business.

2.2 Substantial work expected

The regulations on license and registration under VC Act generally are reasonable. Having said that, the rules require some level of paperwork and subsequent continuous monitoring and control of observance thereof.

2.3 Registration of foreign VC exchange

A foreign VC exchange has two ways for its business to get registered in Japan, i.e., the offshore company itself gets registered or an affiliate/ subsidiary located in Japan registered. To take the first way, VC Act requires that the foreign VC exchange have a VC license in foreign jurisdictions. If it is not so licensed elsewhere, the only possible way is to set up a joint-stock company (Kabushiki Kaisha) and get it registered in Japan.

2.4 Prohibition of Business Non-registered also applies to Foreign VC Exchanges

As written in item 1.4 above, VC Act prohibits VC exchange business operation in Japan without VC Exchange registration. Theoretically, an offshore VC exchange may transact with Japanese residents who voluntarily approach it without being solicited by it. However, the term “solicitation” in the context of “Internet,” is broadly interpreted. Any offshore VC exchange that does not intend to get registered in Japan must effectively prevent all Japanese residents from transacting at its website.

2.5 Timeline

It is said to take three (3) to four (4) months from the start of the discussion with the regulator to file the official application for registration. The applicants are expected to hear from the regulator in a month or two.

3 Requirements

3.1 Minimum capital requirement and minimum financial status requirement

The Act requires VC Exchange has at least JPY 10 million capital and not in the state of insolvency (i.e., liability should not exceed asset plus capital).

From our experience, the capital amount (JPY 10Mln.) is never enough for the necessary setup. Even though the Act allows startup companies to enter this market, such startups virtually need to be injected capital by way of certain reliable/stable financing such as early-stage investment to avoid insolvency.

3.2 Attachment documents to be submitted with registration application:

- Oath declaring that none of the grounds for refusal of registration apply.

- Directors’ Certificate of Residence

- Paper concerning use by director of original family name

- Certificate that directors are under no adult guardianship and have no pending bankruptcy.

- Directors’ resume/CV

- Shareholders Register (top 20), Articles of Incorporation, Certificate of Registration,

- For foreign VC Exchanges: Certificate of Registration in the country of incorporation

- Latest Balance Sheet and Profit Loss Statement

- For companies with Accounting Auditor: Report of Accounting Auditor

- Prospect of profit and loss for three fiscal years from the startup

- Description of VC to be dealt in

- Organization Chart (describing department in charge of Internal Control function)

- Resume/CV of a person responsible for the management of VC Exchange Business

- Internal Rules concerning VC Exchange Business

- Contract forms for execution of VC Exchange Business

- Outsourcing agreement if any part of the VC Exchange Business is being outsourced

- Name of the designated dispute resolution organization, if any, or complaint resolution/dispute resolution

- Miscellaneous

With respect to the item 14, VC Exchanges are generally required to submit more than 20 rules and manuals.

3.3 Local director

The act requires Foreign VC exchange, which operates business through Japanese branches to have a local representative who resides in Japan.

The Act is silent as regards Japanese VC exchange, but we understand that the regulator will require the Japanese VC exchange to have at least one director who resides in Japan.

3.4 Local compliance officer to be stationed in the office

A VC exchange would need to retain a compliance officer and an internal controller who understands Japanese laws (cf. alternatively, both functions may well be served by one person single-handedly).

3.5 Physical office requirement

JFSA requires a VC exchange to have a physical office, not just an office address in Japan.

3.6 Segregation of assets

The Act requires such VC exchange that accepts deposit (in fiat or VC) to segregate its assets from its users’ assets. The VC exchange needs to deposit users’ fiat currency in a bank account under its name that is different from the bank account into which it deposits its operating money. The VC Exchange must segregate its users’ VC from its proprietary VC on the blockchain. The VC Exchange must ensure that each user’s fiat currency/ VC is immediately identifiable.

3.7 Audit

A VC Exchange must undergo an annual audit of its financial statements and segregation of assets.

3.8 Customer identity verification

A VC exchange is obliged, under the Act on Prevention of Transfer of Criminal Proceeds, to verify customers’ identity before opening an account (such authentication is primarily made by sending a restricted-delivery mail to the customer) and set up a robust internal control for anti-money laundering.

3.9 Accountability to users:

A VC exchange must provide adequate explanation to its users for user protection,e.g.:

- Unlike fiat currency, virtual currency is not guaranteed to be convertible to fiat currency,

- any user must be fully informed of its transaction, the handling fees charged, where it can file complaints

- users must be provided receipts by the VC where they deposit money, etc. with the VC exchanges.

3.10 Information security

The VC exchanges must securely control their electronic information system so that their VC and records are protected against constant cyber-attacks.

3.11 Protection of personal information

The VC exchanges must ensure the protection of personal information they obtained.

3.12 Sensitive information

Sensitive information, amongst others, must be securely controlled thus should be handled with extra care.

3.13 Outsourcing

Certain operations may be outsourced to other VC exchanges. Still, the

responsibility remains with the principal thus the VC exchanges must retain authority to inspect and supervise such outsourced.

3.14 Bookkeeping

Each VC exchange must prepare books and keep the record regarding its business. It should also file the business report with JFSA.

4 Procedure for Registration

4.1 Procedure Overview

Generally the registration process would proceed in the following order: (i) discussion with a lawyer, (ii) first meeting with the JFSA, (iii) preparation and submission of draft application documents including internal rules, (iv) comments are received from JFSA, applicants revise such drafts and submit them for further review and comment by the JFSA (the stage (iv) is repeated several times), (v) official submission of the application documents, (vi) further comments from JFSA are received and the application documents are revised accordingly, (vii) The application is officially accepted and registration is made.

4.2 First JFSA meeting

Amongst others, the JFSA requires an exchange to submit the below-listed information at the first meeting.

General Information about the Company

Names of shareholders, the names of directors, the expected number of staff, the expected organizational structure, the name of the accounting firm, the capital amount, the net assets, and the estimated income are required.

Intended Business

The kind of business that is contemplated to be conducted (such as Internet Exchange, OTC, ATM)

Whether there is a leveraged transaction

Names of virtual currencies to be handled

Whether the company will accept deposits of money/VC from users

Intended start time for exchange business

Nature of target users (such as individuals, institutional investors, Japanese residents, etc.)

Background of the Main Shareholder

Example background: “AAA Company is established in year BBBB, located in country CCC and operates DDD business. Net asset of AAA is EEE. The capital of AAA is EEE. AAA would like to set up a VC exchange because [reasons to be described]….”

Background of Directors and Important Officers

Information on the Virtual Currencies to be handled

Name of the virtual currency, unit, presence or absence of the trading market, supplying method, authentication method, usage, total supplied amount, market capitalization, max supply, current market price per unit, the existence of an issuer, risk related to such VC.

5 Conclusion

The setup is not without pains as discussed above. However, the regulatory environment in Japan is seen to be, and in fact still is, a robust one, and more entrepreneurs are swarming. Currently, there are 16 licensees and 90 more prospective applicants said to have approached JFSA to apply next in queue. The Act and the surrounding regulations have not been set up, except for JFSA’s series of discussions over the year with VC exchanges that were starting up. For further development of VC, business self-regulation is being awaited across the globe where public vs. private discussion alone would foster such workable self-regulation in the industry.

Initial coin offerings (“ICO“) have been one of the global hot topics followed with growing enthusiasm, but what regulations are applied to ICO is still unclear in most countries. Some issuers sell coins by way of ICO unknowing of regulations in the countries that may be relevant or even applicable, only to take serious regulatory risks. In Japan, most ICO coins are regulated under the so-called “Virtual Currency Act” (the provisions in the Payment Services Act concerning virtual currencies—”VC Act” or the “Act”) which took effect in April 2017. Some coins might be regulated under other laws. Below are general guidance on regulations and laws which you would need to consider when you contemplate an ICO in Japan.

Conclusion

| (A) VC Act (a) If ICO coins are deemed “Virtual Currency” (“VC“) as defined in the Act, only the registered Virtual Currency Exchange Business Operators (“VC Exchange Business Operator“) are authorized to handle such an ICO. (b) The Japanese Financial Services Agency (the “JFSA“) presumes most ICO coins to fall under statutory “VC.” (c) Even a registered VC Exchange Business Operator cannot deal in all existing VCs. The VCs to be handled should be reported to and approved by the Japanese Financial Services Agency. (e) ICO issuer has three choices when selling ICO coins. The first such choice is to get registered as VC Exchange Business Operator and sell tokens itself. The second is to delegate sales of ICO coins to a third party registered VC Exchange Business Operator. The last option is not to sell ICO tokens to Japanese residents (B) Financial Instrument Exchange Act (the “FIEA”) (a) The fund regulations pursuant to the FIEA (the “FIEA Fund Regulations”) will apply, if ICO constitutes “collective investment schemes (fund),” i.e., a scheme that is (i) to collect money from others; (ii) to invest in a business; and (iii) to pay dividendsto holders thereof. (b) ICO coins which do not satisfy the test in (B)(a) above are not regulated by the FIEA Fund Regulations. We believe that the coins such as Bitcoin and Ether do not constitute “funds” under the FIEA. (c) In principle, those funds that solicit not for “fiat,” but for “VC” will not constitute “funds” under the FIEA. (C) Consumer Protection Act and Civil Code (a) From the general consumer protection point of view, appropriate explanation to the investors is required irrespective of whether such ICO coins are regulated by the VC Act, by the FIEA, or by neither thereof. |

2. Virtual Currency Act

2.1 If ICO coins are deemed “VC” under the VC Act, only the registered VC Exchange Business Operator may sell VC on a regular basis

According to the VC Act, only such a VC Exchange Business Operator as has been registered pursuant to the Act may carry out any ICO, to the extent that (i) such ICO is in respect of the VC as defined in the Act; and (ii) the subscriptions solicited are paid in cash or other VC (which act of “sale and purchase of VC or exchange of a VC into another” “as carried out on a regular basis” is prescribed for the registered “VC Exchange Business Operators” by the Act).

2.2 Even the registered VC Exchange Business Operators may not be authorized to handle the entire universe of existing VCs. VCs to be dealt in should be reported to and approved by the JFSA.

The VC Act requires the registered VC Exchange Business Operator to report to the JFSA a list of coins it contemplates to deal in, which list is after that reviewed, with some coins possibly being screened out.

We are still discussing with the members of the self-regulatory organization and with the JFSA what coins are appropriate to be dealt by the registered VC Exchange Business Operators.

2.3 Currently the JFSA deems most ICO coins to be VC

Currently, the JFSA deems most ICO coins to be VC.

VC Act defines “VC” as the first set of definitions Bitcoin most typically meets (such coins collectively are “Type I VC“). The second set of the VC definitions are characterized by the fact that such coins may be exchanged for the above-mentioned Type I VC “with unspecified persons as the other party” (such coins collectively are “Type II VC“). The VC Act excludes from its application coins that are linked to any

fiat currency. The coins that are linked to any fiat currency are regulated by yet another regulation.

What this “unspecified person” means in the context of Type II VC definition is somewhat unclear. However, the FSA seems to think that (i) coins are deemed to be VCs if such coins have a possibility to be exchanged with Type I VC in the future and (ii) coins are deemed not to be VC, where, for example, such coins are structurally prevented from being exchanged with Type I VC. As most ICO coins are contemplated to be listed in the exchanges and to be exchanged with Bitcoin etc., we

believe most coins would be deemed to constitute regulated VC from the JFSA’s viewpoint.

2.4 Three Ways to sell ICO coins

ICO issuer can choose out of three ways to sell its ICO coins.

The first method is to get registered as VC Exchange Business Operator registration and sell tokens by itself. It takes about 6 months to get registered, and some costs are incurred. Please see our earlier memo, “Guidance Note on the Japanese Virtual Currency Legislation and Overview on Registration Requirement thereunder” for more details of the registration.

The second method is to delegate sales of ICO coins to a third party registered VC Exchange Business Operator. Currently, there are 15 registered exchanges in Japan. We understand that they are asked to treat ICO tokens every day, and they accept only tiny percent of such offers. Thus, to negotiate with the registered exchange might not be so easy. Since many new businesses are applying to the JFAS now, the

situation may change in the future.

The third method is not to sell ICO coins to Japanese residents. If you exclude Japanese residents from purchasing ICO tokens, we believe that you do not need to take the VC Exchange Operator license.

3. FIEA and the Fund Regulations

3.1 Bitcoin and Ether do not fall under the definitions of securities

For the FIEA to apply, the case must involve either “Negotiable Instruments/Securities” or “Derivatives” as defined therein. These terms are defined by a fixed list of items, each of which is also defined. Common virtual currencies such as Bitcoin and Ether are included in neither “Negotiable Instruments/ Securities” nor “Derivatives.” Hence, as a general rule, the act does not apply to the sale and purchase or exchange of a VC such as an ICO.

3.2 Collective Investment Scheme is regulated by the FIEA

Having said that, amongst the statutorily-defined items of Securities, the term “collective investment schemes (fund)” is a broad and diverse concept. Certain ICOs seem to fall under such “collective investment schemes,” specifically, where an ICO is (i) to collect money from others, (ii) to invest in a business, and (iii) to pay dividends to holders. Such a structure most likely invites the application of the FIEA Fund Regulations. The FIEA Fund Regulations are generally stricter than the

regulations on VC under the VC Act, and you should be careful with such possible applications to your ICO.

When coins are offered in exchange for payment in Bitcoin or Ether, the FIEA Fund Regulations are unlikely to come into play because Bitcoin and Ether are not “money” under Japanese law. However, if someone sells Bitcoin and Ether in exchange for cash to investors and then collect such Bitcoin and Ether from the investors as an investment to a fund, the chain of actions as a whole may be deemed to constitute

collecting “money” and, thus, may be regulated.

3.3 Certain funds such as real estate funds might still be regulated even if they collect

investment solely in VC.

You need to consider yet another regulation if money or VC collected by way of ICO is invested in a certain specific asset class. For example, some ICOs that invests money or VC in real estate businesses might be regulated under the Act on Specified Joint Real Estate Ventures in Japan. Since the Act on Specified Joint Real Estate Ventures does not distinguish VC from money, ICO might be regulated even if the ICO collects investment via Bitcoin or Ether.

4. Consumer Contract Act and Civil Code

Where neither the VC Act nor the FIEA Fund Regulations reach, sellers are still not entirely at liberty to design an explanation of their products.

For instance, any consumer is entitled to rescind the manifestation of his/her intention to enter into a transaction in which a soliciting business operator has made misrepresentations as to the material facts, intentionally omitted an explanation of material facts, or provided conclusive evaluations. Accountability under the Civil Code (etc.) will also come into question. Any products offered, irrespective of whether they constitute VC, should without exception entail reasonable explanations.

From the consumer protection point of view, explanations made for most of the arguably fraudulent coins do not seem to amount to clear-cut “false statements” or “conclusive evaluations.” However, there may still be room to argue that the “intentional omission of material facts” has been committed. It may justify further contemplations by the legislator or self-regulatory organization of the minimum disclosure standard, i.e., list of material facts/ important matters.

Should you contemplate ICO, we recommend that you get ready for adequate disclosure to the investors

(1) SEC Chairman Jay ClaytonのICOレター (Dec. 11, 2017)

https://www.sec.gov/news/public-statement/statement-clayton-2017-12-11

Statement on Cryptocurrencies and Initial Coin Offerings

(2) Dec. 11, 2017

Company Halts ICO After SEC Raises Registration Concerns

https://www.sec.gov/news/press-release/2017-227

Sample Questions for Investors Considering a Cryptocurrency or ICO Investment Opportunity

- Who exactly am I contracting with?

- Who is issuing and sponsoring the product, what are their backgrounds, and have they provided a full and complete description of the product? Do they have a clear written business plan that I understand?

- Who is promoting or marketing the product, what are their backgrounds, and are they licensed to sell the product? Have they been paid to promote the product?

- Where is the enterprise located?

- Where is my money going and what will be it be used for? Is my money going to be used to “cash out” others?

- What specific rights come with my investment?

- Are there financial statements? If so, are they audited, and by whom?

- Is there trading data? If so, is there some way to verify it?

- How, when, and at what cost can I sell my investment? For example, do I have a right to give the token or coin back to the company or to receive a refund? Can I resell the coin or token, and if so, are there any limitations on my ability to resell?

- If a digital wallet is involved, what happens if I lose the key? Will I still have access to my investment?

- If a blockchain is used, is the blockchain open and public? Has the code been published, and has there been an independent cybersecurity audit?

- Has the offering been structured to comply with the securities laws and, if not, what implications will that have for the stability of the enterprise and the value of my investment?

- What legal protections may or may not be available in the event of fraud, a hack, malware, or a downturn in business prospects? Who will be responsible for refunding my investment if something goes wrong?

- If I do have legal rights, can I effectively enforce them and will there be adequate funds to compensate me if my rights are violated?